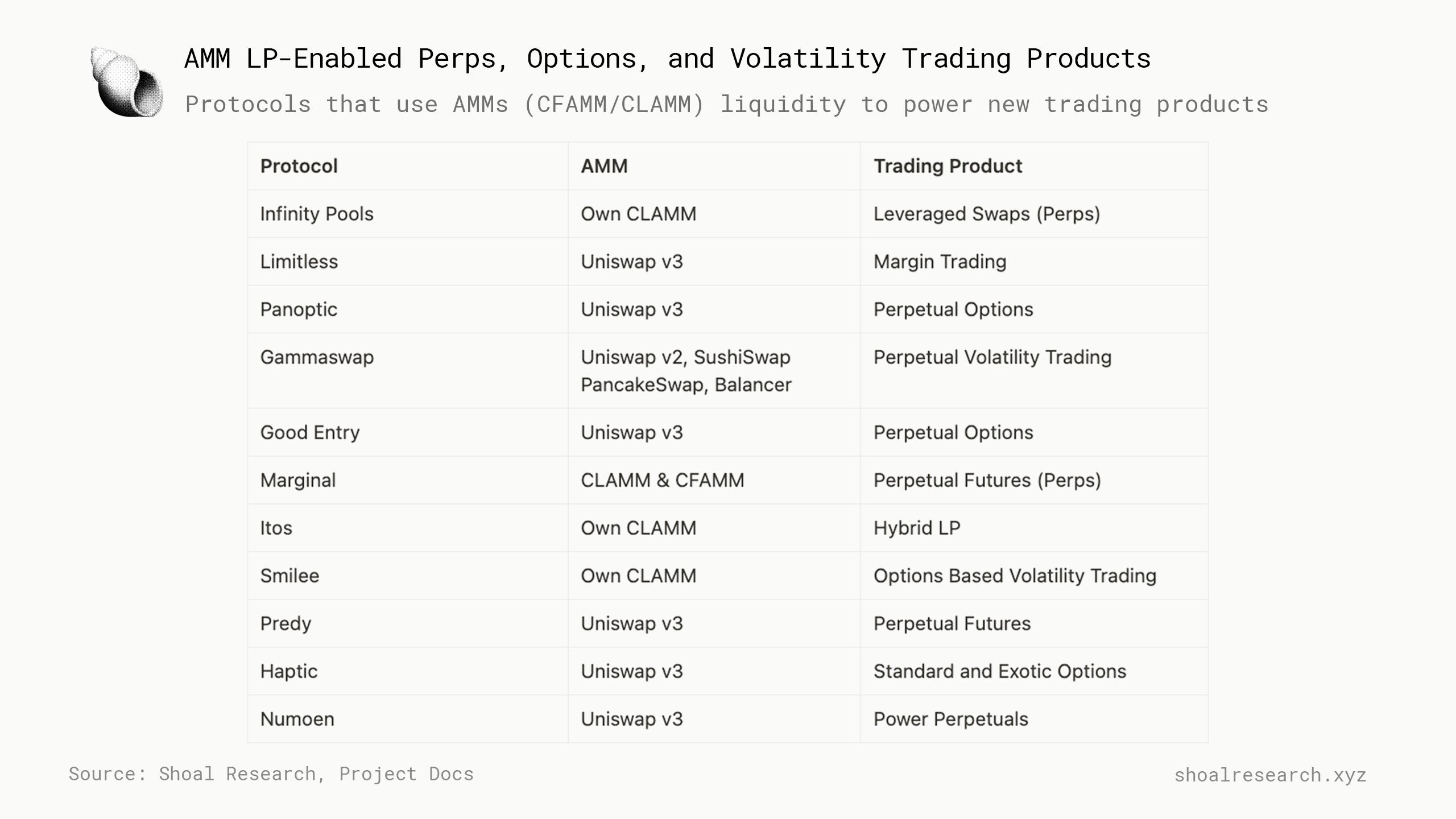

AMM LP-Enabled Perps, Options, and Volatility Trading Products

Protocols that use AMMs (CFAMM/CLAMM) liquidity to power new trading products

Special thanks to Pablo, Matthieu, Jesper, Brandon, and Terence for feedback and input on this new DeFi mechanism.

Intro

For some, an automated market maker (AMM), a type of Decentralized Exchange (DEX), is the only way traders can exchange certain assets of interest. Centralized exchanges often exclude these assets due to factors like low liquidity and dependence on traditional market makers. Whether it be Uniswap, Curve, Balancer, or even aggregators like MetaMask and 1inch, AMMs have facilitated trillions of dollars of value since inception just a few years ago. DEX's permissionless design makes them an ideal platform to trade low liquidity or long tail assets (assets not included in top trading volumes) since anyone can create a market for new assets. Unlike a traditional CEX, which has to integrate assets manually, AMMs allow seamless deployment and trading of any ERC-20 token as long as someone provides liquidity. This is because AMMs allow anyone to deposit assets and become a market maker, as opposed to needing to be an institutional entity like in traditional finance (TradFi). Market makers add liquidity through buy and sell orders on exchanges to ensure that users can execute trades even when no other users are present. They earn money by capitalizing on the spread, which is the difference between the buying and selling prices.

However, most spot* AMMs are extremely vanilla and typically only support buy and sell orders. Other spot AMMs and aggregators offer advanced features like limit orders and deep liquidity (enough liquidity for large entities to trade). However, they still cannot convert their liquidity into other trading primitives. DeFi primitives are the simplest building blocks.

“Spot markets are also referred to as “physical markets” or “cash markets” because trades are swapped for the asset effectively immediately.” - Investopedia

It is often said in the product world that products need a 10x improvement to displace incumbents and experience significant adoption. The introduction of DEXs like Uniswap, solved a unique liquidity issue by allowing users to create a market for any ERC-20 at lightning speed.

DEXs like Uniswap and Curve have been battle-tested long enough to be used as primitives for other products.

DeFi primitives are the essential “building blocks” that can be combined to create DeFi functionalities of a higher order. - Binocs

Similar to the DEX spot markets, other trading products like Perpetual Futures (Perps) and Options are also hyper-competitive and still dominated by CEXs with regard to trading volume. Although CEXs dominate, there still is a large opportunity for Perps, options, and other trading products to grow exponentially by harnessing the composability of DeFi, the stacking of DeFi “Legos,” or applications that can build upon each other.

Most on-chain Perps and derivatives have few assets, use oracles, and are susceptible to liquidity issues. Without sufficient liquidity, derivative exchanges are unable to function and attract more users, which is the so-called chicken-egg problem. Here lies a sizable opportunity for the 10x "Uniswap" moment for on-chain derivatives by enabling leverage, Perps, and option trading products for any asset. To make this possible, new protocols are using concentrated and constant function AMM liquidity to power new trading products (leverage, Perps, and options). Simply put, protocols harness AMMs like Uniswap as a liquidity primitive to create new trading products.

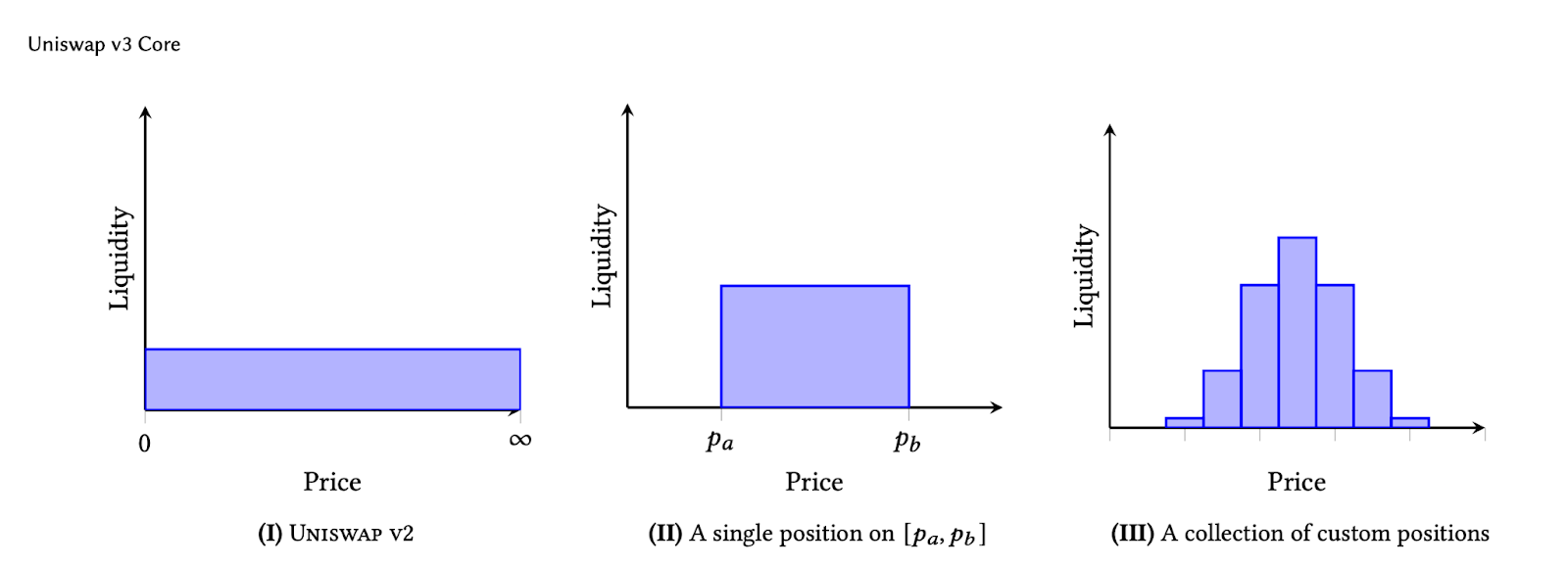

Constant Function AMM: Liquidity is typically spread across a full range of prices infinitely (Uniswap v2, Balancer).

Concentrated Liquidity AMM: Liquidity is concentrated to a price range (Uniswap v3).

Perps and Options Uniswap Moment

The killer use case with AMM-powered trading products is being able to create Perpetual futures (Perps), Hybrid-Options, and other volatility markets for illiquid and newly deployed assets. $PEPE, during its boom, soared to a multi-billion dollar market cap in just a few weeks. During this period of extreme volatility, traders repeated the continuous question:

“Where can I long $PEPE”

Although PEPE's popularity has grown immensely, garnering billions in volume and turning into a household name, there were initially only spot markets to trade the asset. Shortly after a few weeks, some opportunist exchanges enabled Perpetual (Perps) trading and continued to be the only sources even up to now. Even among some of the exchanges that enabled $PEPE trading, many traders believed there were issues with handling liquidations and payouts, a core concern in Perpetual exchange design. With AMM-powered volatility products and derivatives, there is an opportunity for on-chain market makers known as Liquidity Providers (LPs) to market-make options and Perpetuals at token launch, akin to Uniswap.

There is plenty of speculative demand for crypto assets, especially regarding leverage. Outside of leverage, these products provide great tools to hedge LP positions on assets. Hedging is opening another trade to lower the initial investment risk deliberately.

Perpetual Trading Products

Many on-chain Perpetual contracts (Perps) rely on oracles, which can be easy to manipulate for long-tail assets. Oracles take off-chain data and make it accessible on-chain for protocols to use, commonly used for price feeds. Ever wonder why only a few assets are supported on Perp Decentralized Exchanges? Most on-chain Perps and options platforms offer just a handful of assets geared towards deep liquidity and utilize an external oracle for the pricing mechanism. Liquidation risk is also a significant issue since managing liquidations depends on accurate oracles and ensuring that trades can be liquidated to meet collateral requirements in a timely manner. In other words, liquidations need to occur seamlessly to ensure that collateral is available to cover trades. With concentrated liquidity AMM (CLAMM) powered trading products, oracle, and liquidation risks are typically eliminated, as the liquidity is borrowed from a predefined LP range.

By adopting this approach, the risk is also predefined for the trader and limited to the parameters set by the exchange protocol for closing positions. Many AMM LP-enabled protocols employ a Perpetual mechanism for trade duration, which allows the trade duration to roll over as long as the fees are paid to keep the position open.

AMM and LP Fees

CLAMMs (Concentrated Liquidity Automated Market Makers) and CFAMMs (Constant Function Automated Market Makers) constitute dual-party markets involving Liquidity Providers (LPs) and traders. For traders, the experiences across AMM products are mostly similar. Conversely, many exchanges strive to optimize the liquidity-providing experience since it frequently results in losses. In numerous instances, LPs need additional incentives to become profitable.

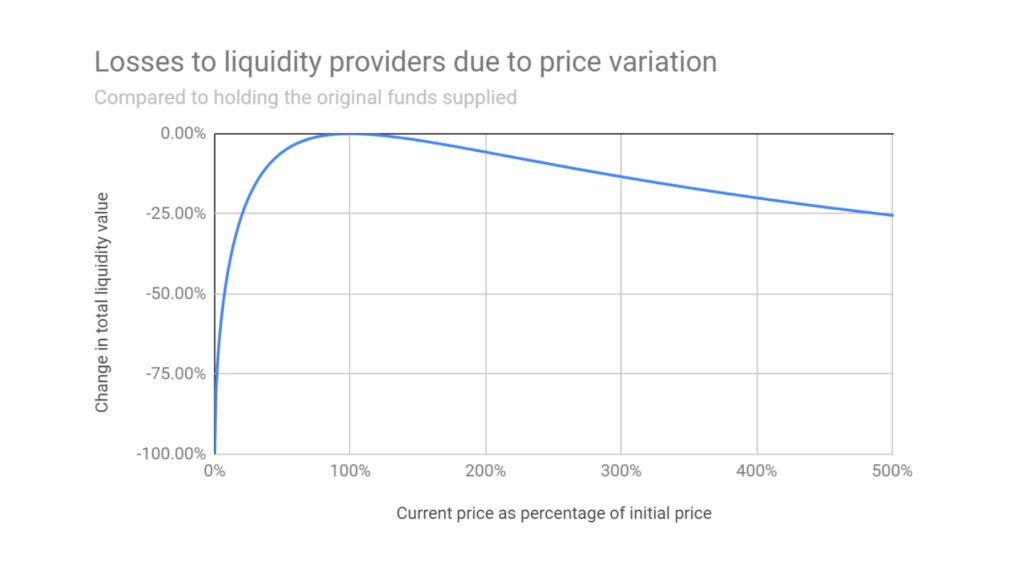

Many Liquidity Providers add liquidity to AMMs based on the assumption that they will receive fees sufficient to offset impermanent loss (IL), a theoretical loss incurred by LPs when the price of the deposited tokens changes. It is also important to note that all LPs are not benchmarking against a HODL strategy. One of the core improvements in the concentrated AMM liquidity derivatives model is that LPs are now compensated in volatility, not just trading fees. This innovation introduces a new dimension to the rewards of liquidity provision.

For some AMM-powered derivatives like infinity pools and Panoptic (Panoptic Option Sellers), LPs can generate fees when their LP is within range, and commission fees when both in and out of range. When the LP token goes out of range, it can be used for the protocol's volatility product, whether it be leverage, margin, or options trading. This architecture allows for enhanced yield for LPs who usually have a subpar experience when providing liquidity.

AMM LP-Powered trading products - How do they work?

The current protocols offering AMM-powered trading derivatives abide by the simple assumption that providing LP in a CLAMM is akin to short puts. In other words, the liquidity-providing payoff structure is mathematically similar to selling put contracts. Perpetual and volatility trading protocols are able to structure trading derivatives and strategies around this concept, creating leverage, Perps, Perpetual options, and other structured products.

Protocol Landscape

Currently, there are a handful of protocols aiming to leverage CFAMM and CLAMM liquidity for trading purposes. Among them, a few trading products exist, including Leverage and Margin trading, Option products, Perpetual futures, and more. As nascent as the concept may be, many builders find opportunities to fill the liquidity and asset gap for major and long-tail assets within trading products. The following table shows the protocols, their liquidity AMM, and the trading product created:

Let’s look further into the mechanisms and design.

Perpetual Option Mechanism Design

Protocols like Panoptic and Smilee utilize concentrated liquidity LP to power their trading products, specifically Perpetual options and volatility trading, respectively. Among the handful of protocols leveraging existing AMM concentrated liquidity, each presents a slightly different architecture and implementation in how they are crafting trading products.

At a high level, protocols draw concentrated liquidity from AMMs like Uniswap v3, or their own AMM and permit traders to borrow these assets. Traders then redeem the underlying LP token for a single asset, simulating a long or short position constrained by the range of the concentrated liquidity. Due to the nature of concentrated liquidity positions, when out of range, they always consist of 100% of one of the two assets in the pair (e.g., USDC/ETH). Since LPs expect 100% of one of the two assets in the pool, traders pay a fee to borrow and redeem the LP pair, receiving one of the assets. Depending on their trading strategy, they can sell the redeemed token, turning it into a directional bet.

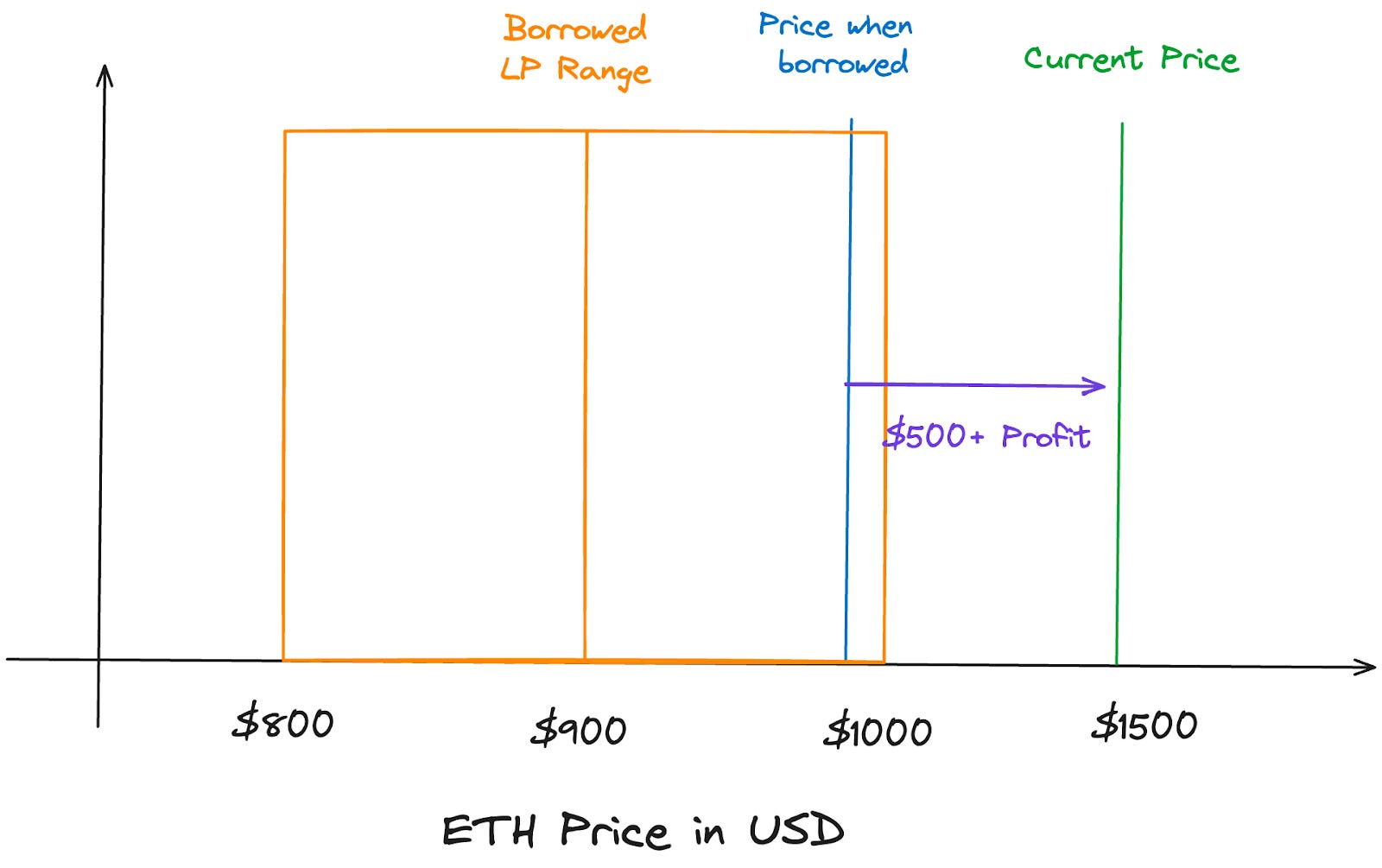

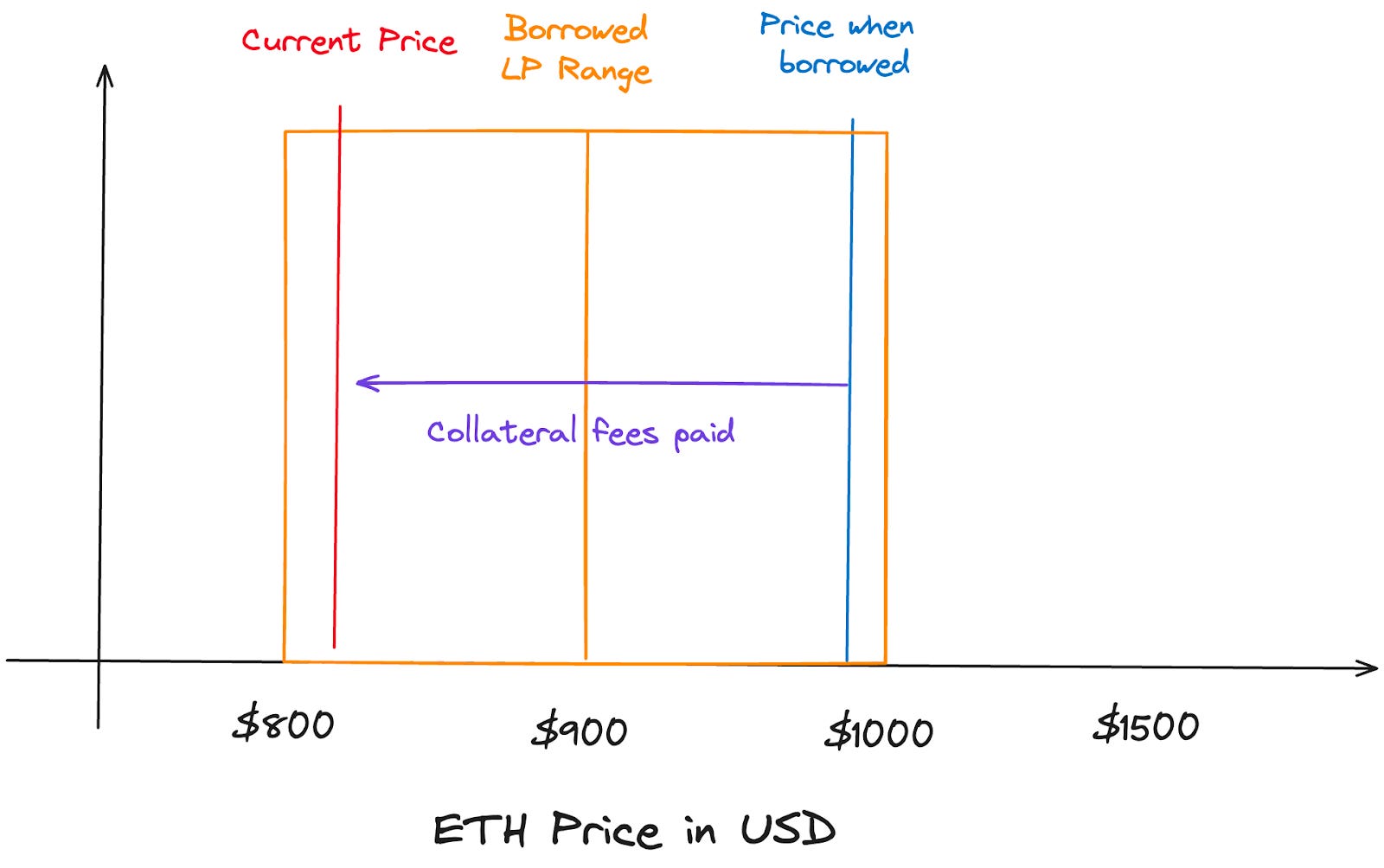

Long ETH example

For a Perpetual options example, let's say a trader wants to borrow a USDC/ETH LP token where the price of ETH is $1000. The trader wishes to go long on ETH, so they borrow an out-of-range USDC/ETH LP token below the current price, which would be worth $1000 of USDC. The LP token is valued at $1000 USDC because the current price has moved to the right side of the range, leaving the LPer (options seller) with 100% USDC. The option buyer's strike can be considered as the midpoint of the LP range; we'll use 900 for this example. Since the trader is long, they redeem the LP token worth $1000 USDC and swap it for 1 ETH, also worth $1000. If the price of ETH moves up to $1500, and since ETH is now valued more than what the options buyer purchased it for, they can exercise the option by selling the 1 ETH for $1500. This amount is sufficient to pay back the borrower and yield an additional $500 profit. The options buyer only repays $1000 to the LP since that is the end of the range in which they are providing liquidity.

Protocols typically abstract most of the complexity from this experience. Users may expect to deposit collateral to cover position funding, select position duration (if included), strike price, and trade direction.

Long ETH trade cont..

If the trade doesn't go as planned and ETH goes down to $800, which is out of the LP range in the opposite direction, they will now owe 1 ETH instead of USDC. Since the borrower still owes 1 ETH to the lender, they need to find a way to obtain 1 ETH to repay the loan. If the value of 1 ETH is $800, the borrower needs to use $800 worth of USDC to purchase 1 ETH to settle the debt.

The DEX manages the underlying assets for protocols like panoptic to ensure LPs get paid. Instead of paying a premium to purchase the option upfront, Panoptic requires users to have starting collateral in their wallet to cover a streaming fee similar to a funding rate. Collateral is needed to guarantee that the fee can be paid. The fee is based on realized volatility in the underlying Uniswap pool and liquidity utilization to determine how much the option buyer should pay the seller (LP). Traders positions will close when they stop paying the funding fee or it exceeds their collateral.

In both examples, the option seller will take constant streamed fees for the position to remain open. This is a general overview pertinent to panoptic as each protocol has different methods for managing liquidity, offering leverage, calculating collateral, premium, and funding fees.

From a birds eye view, trades are two-sided, where LPs deposit their LP token into the said protocol and earn volatility fees, where traders can open positions. LPs are incentivized to provide liquidity because they get bonus yield, which is more than they would've gotten otherwise. One of the core issues with LPs in AMM are they are not paid high enough in fees to compensate for risk. Lastly, profitable traders can exercise their position in profit or continue to pay the LPs a funding rate to keep the trade open perpetually.

Perpetual Future Mechanism Design

For Perpetual platforms like limitless or InfinityPools, the mechanism is similar to Perpetual-options. However, users can deposit collateral, which will be combined with borrowed LP. Depending on the distance from the spot price determines the required collateral and leverage. Similar to the Perpetual options products, if a trader borrows an LP token below the range they can sell for one of the underlying tokens, creating a directional leveraged bet. The design mechanism is very similar to the prior example, the major contrast is the users deposit collateral, which is used to cover the max loss of a trade moving in the opposite direction. Both limitless and InfinityPools boast potential hundreds to thousands of X-leverage again determined by the distance from the range to the current price. If traders lose on a trade instead of being liquidated, the protocol closes their position and pays the collateral back to the LP to make the Perp sellers LP position whole.

Market Opportunity - Crypto Trading Derivatives

TradFi Market Size

The U.S. equity markets dominate globally, accounting for over 42.5% of the $108.6 trillion global equity market cap in 2023, translating to a massive $44 trillion, as per Sifma Asset Management.

TradFi Derivatives Landscape

The derivatives market is estimated to exceed $1 quadrillion in notional value at its upper end, though some argue this valuation might be inflated as per Investopedia. This astronomical figure, on the higher side, incorporates the notional value of all derivative contracts.

A significant disparity exists between the notional value and the actual netted value of derivatives, with the numbers being $600 trillion and $12.4 trillion, respectively, as of 2021.

Derivative trading in traditional finance is magnitudes larger than spot trading. This is the same in crypto, but the majority of volume is on CEXs.

Bitmex, another CEX, changed the crypto trading landscape in 2016 when they launched their Perpetual (Perp) trading instrument, the Perpetual XBTUSD Leveraged Swap. Their new product allowed users to trade Bitcoin (XBTUSD) with up to 100x leverage. The contract doesn’t expire; longs pay shorts, and vice versa. As the largest traded instrument in crypto, this product expanded from just centralized exchanges and exists in various decentralized versions: DYDX, GMX, Synthetix, and others. Perp protocols facilitate hundreds of millions in trading volume per day and are the primary derivative trading product in crypto today since they offer high leverage. This is a vast shift from traditional finance, where options dominate the derivatives landscape.

Crypto Spot Vs Perps

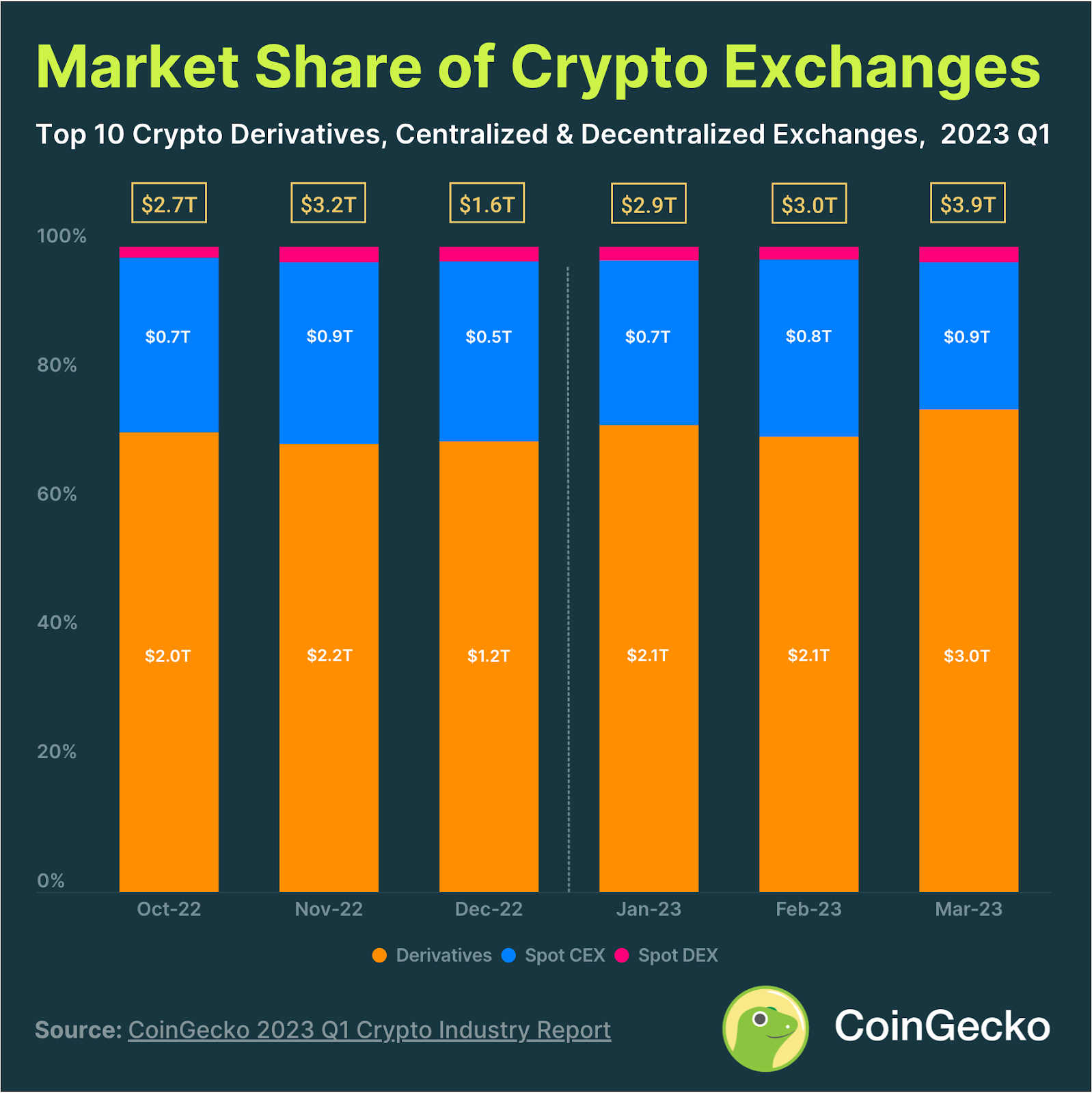

In the first quarter of 2023, the crypto market witnessed a significant dominance of derivatives, accounting for 74.8% of the total trading volume of $2.95 trillion. Centralized crypto exchanges (CEX) and decentralized exchanges (DEX) spot trading trailed behind with 22.8% and 2.4% market shares, respectively. Notably, centralized crypto derivative exchanges like Binance, Upbit, and OKX led the market. While derivatives volume saw a remarkable quarter-on-quarter growth of 34.1%, spot CEX and DEX recorded growth rates of 16.9% and 33.4%, respectively, per Coingecko 2023 Crypto Derivatives report.

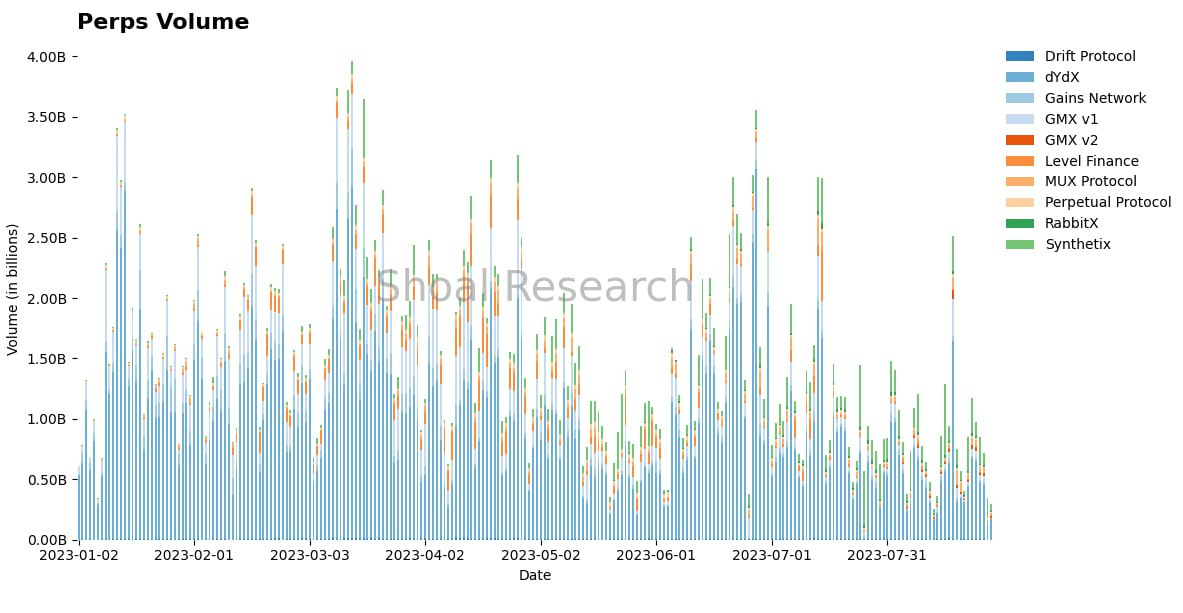

As of July/2023 PREP, 74% of all crypto trading volume in July was via leverage.

(Figure below)

Innovative volatility trading platforms like Panoptic, Infinity Pools, Smilee, and others push the needle by providing oracle-free, liquidation-free, and even, in some cases, offer significant leverage. Powered by concentrated liquidity, AMM LP trading products remove some prominent weaknesses like managing oracles and liquidations.

Risks

As exciting as these products may be, risks still come into play. The most notable is smart contract risk. Since all the AMM-LP powered trading products control the LP token or require deposits, there's possible smart contract risk if there is an exploit or bug.

Credit liquidity Risk

Additionally, the economic design mechanisms are not without concerns. The Gammaswap team has interrogated the feasibility of developing on Uniswap v3 and CLAMMs due to what they define as "credit liquidity risk." This risk pertains to the possibility of Liquidity Providers (LPs) being unable to pay out long positions or vice versa, often due to over-leverage in the form of liquidation issues. Since concentrated liquidity, Automated Market Makers (AMMs) like Uniswap have areas or "ticks" with low liquidity, prices moving out of range could cause excessive slippage, even for stable pairs. Gammaswap is opting to build on the constant function model, viewing it as a more robust liquidity primitive.

With Uniswap v3, there may not be enough liquidity to fulfill the gains made by LPs. Unlike traditional finance, where the Federal Reserve can step in to inject liquidity, there is no analogous entity in the DeFi space. Furthermore, the absence of oracles, which are traditionally used for liquidations, adds to the complexity of this issue.

Panoptic addresses the credit liquidity risk issue by requiring pool creators to deposit a small amount of both tokens at full range, which panoptic traders cannot remove. The initial deposit ensures there's some liquidity across all prices.

Complexity and User Adoption

Perpetual Futures (Perps) have proven to be much simpler for crypto investors to understand. They operate through two mechanics: long and short positions, which traders can open with a simple click of a button. In contrast, with Options and potentially Perpetual Options, the additional complexity introduced by factors such as Greeks, strike prices, and other traditional option knowledge may hinder user adoption. This is particularly likely among retail investors, who are often the first to adopt new trading instruments. Moreover, introducing volatility trading adds even more complexity to the user experience. Since the crypto space already faces challenges with user adoption, some of these robust but complex products could encounter difficulties gaining traction due to their financial intricacy.

Conclusion

Perpetuals and Options have found a niche within the crypto space, but it's only a matter of time before they scale into the fully-fledged products that traders and LPs are seeking.

Over the next few months, many of the protocols mentioned will be launching new trading instrument betas, as well as live products. The next level of improvement in on-chain derivatives, including Perpetuals and options, will be the introduction of the ability to go long (or short) on any asset with leverage. The "where can I long PEPE" question will be answered in the form of leveraged liquid trading avenues for mid to long-tail assets.

AMM-powered trading products are paving the way for a new paradigm of trading and could potentially enable new DeFi primitives that power other protocols. This includes options, Perpetual contracts, volatility trading, and other leverage-based products. The new wave of trading will offer an enhanced experience that could even rival the current incumbents in the market.

Sources

Announcing the Launch of the Perpetual XBTUSD Leveraged Swap | BitMEX Blog

What are DEFI Primitives & Where DEFI Primitives are used in Financial services | Binocs

Cash Market: Definition Vs. Futures, How It Works, and Example

Gamma transforms: How to hedge squeeth using Uni V3 | by Guillaume Lambert

https://limitless.gitbook.io/limitless/intro/participants/liquidity-providers

Not financial or tax advice. The purpose of this newsletter is purely educational and should not be considered as investment advice, legal advice, a request to buy or sell any assets, or a suggestion to make any financial decisions. It is not a substitute for tax advice. Please consult with your accountant and conduct your own research.

Disclosure. All of my posts are the authors own, not the views of their employer.