Liquid Restaking Tokens: A new Frontier for Yield

An Overview of liquid restaking tokens on Eigenlayer

An Introduction to Proof-of-Stake, Staking, and Liquid Staking

Throughout 2023, liquid staking and the primitives surrounding it has permeated all parts of the crypto ecosystem . This rise to popularity of the infrastructure around the Proof of Stake (PoS) consensus mechanism really took off with its integration at the protocol level on Ethereum during September 15, 2022—referred to as the “Merge”. The transition from the traditional Proof of Work (PoW) mechanism to PoS represented a paradigm shift in Ethereum consensus, allowing users to derisk the ability to provide (and price) Ethereum crypto-economic security. This enabled the growth of staking, the emergence of restaking, and the introduction of a new class of assets–liquid restaking tokens.

Understanding Proof-of-Work and Its Limitations

Before delving into PoS, it's instructive to examine PoW, the pioneering consensus mechanism that continues to secure Bitcoin. At its core, consensus for blockchains refers to the underlying mechanism that enables transaction verification without relying on a centralized authority. Typically, consensus requires agreement from at least ⅔ of the network's nodes on its current state. This helps secure the network and confirm the updated history of transactions, also known as a state change.

Under PoW, this consensus is achieved through mining. Miners utilize computational power to solve complex mathematical puzzles. The first to solve these equations verifies the next block, adding it to the blockchain, and in return, earns a reward. This process is resource-intensive, making it a race where participants must consume large amounts of energy for potential rewards.

PoW also plays a pivotal role in transaction validation, preventing malicious actors from double-spending—a scenario where one user attempts to spend the same funds multiple times. However, achieving this in PoW requires maintaining control over 51% of the network, an expensive feat given the hardware and energy costs associated with this consensus mechanism. If an entity does achieve this, they could influence the consensus, posing a considerable risk to the network’s security. In such cases, the only solution to rectify the attack lies in a hard fork. Combating double-spending preserves blockchain's promise of immutability, decentralization, and trustworthiness.

Embracing Proof-of-Stake: A Shift towards Sustainability for Consensus

PoS addresses the same core objective as PoW—validating and adding new blocks through consensus. It does so with greater efficiency and sustainability. Unlike PoW, which relies on energy-consuming computational tasks, PoS relies on validators who 'stake' an asset capital as collateral. To enter the validator set in the beacon chain and participate in validation activities, stakers must deposit a minimum of 32 ETH. Their staked amount acts as a deterrent against malicious activities, as any misdeed could result in a loss of their staked funds and forced exit from the beacon chain–a process known as slashing. The slashing penalty scales with the number of validators slashed within a given time period leading to greater losses for those validators who were slashed as a means to deter collusion between multiple validators at the same time.

The difference between PoW and PoS security mechanisms is substantial. While PoW deters malicious activity through resource expenditure (i.e. the cost of owning and operating a majority of nodes), PoS imposes direct financial penalties to stakers as a means to decrease the computational overhead of securing the chain.

Liquid Staking: Innovating on Composability in the PoS Landscape

The PoS realm had seen numerous innovations to additionally benefit stakers’ potential to earn yield. However, one glaring challenge remained, composability. Initially, stakers couldn't easily withdraw their stake, and there was little incentive to do so given the rewards. Liquid staking tokens (LSTs) emerged as the answer, enabling users to engage with DeFi without compromising on their exposure to staking yield.

Throughout the past year, we’ve witnessed significant growth in LSTs, yet there remain challenges and potential new frontiers to further expand adoption of the vertical by the greater crypto ecosystem..

Slashing is the greatest risk which holders of LSTs are exposed to besides price depegging. As discussed before, slashing imposes a permanent penalty on slashed validators, burning their ETH and exiting them from the beacon chain. This does not necessarily always impact the value of an LST token, however it does impact the amount of ETH redeemable by the token holder. As a result, correlated slashing events in which a significant amount of ETH is removed from the validator set of a liquid staking provider could incite skepticism on the solvency of the asset, leading to sell pressure on that LST and further inciting a depeg event.

Numerous companies are striving to improve the liquid staking experience by offering innovations like reduced bond requirements, distributed validator technology (DVT), and trusted execution environments (TEEs), all with the aim of reducing the risks around slashing and making staking safer. It will become increasingly important to utilize such tools within the validator infrastructure of liquid staking providers as more use cases for LSTs in the DeFi ecosystem make solvency for LSTs even more important..

Concurrently, there's a rush to satisfy the appetite for diverse yield opportunities, be it through DeFi, incentive mechanisms, or innovative products. One such paradigm that has risen to the main stage is restaking. Restaking is specifically designed to reflect the ETH PoS crypto economic design and iterate on it to reduce the barriers of bootstrapping PoS systems while allowing stakers to earn additional revenue on their assets.

Restaking and the Advent of Actively Validated Services

Extending Ethereum’s POS Security

Ethereum’s PoS consensus mechanism offers a unique advantage: it's programmable and scalable security via cryptoeconomic value. This security, intrinsic to Ethereum, extends seamlessly to all of the protocols that are secured by the underlying continuity of the beacon chain as a byproduct. This is a diverse array of smart contract protocols, ranging from decentralized exchanges (DEXs) to NFT marketplaces. However, until recently, this robust security framework didn't wasn’t able to innately extend itself to other applications or distributed systems such as bridges, sequencers, data availability layers, or other blockchains that required some other form of consensus. Systems like these have traditionally been tasked with bootstrapping their own consensus mechanisms to safeguard their operations, a challenge exemplified by platforms like Axelar and its native PoS network.

Restaking: Bridging the Security Gap

Addressing this gap in extendability of security provisioning led to the inception of restaking—a pioneering concept that allows staked assets on Ethereum to bolster the security of arbitrary distributed systems. EigenLayer, the first restaking protocol, coined the term "Programmable Trust" to describe this mechanism. More intriguingly, the distributed systems benefiting from this trust mechanism are termed Actively Validated Services (AVSs).

EigenLayer: Amplifying Commitments and Security

At its core, EigenLayer operates as an amalgamation of smart contracts and off-chain software, amplifying the commitments a validator or other external node operator can undertake. This enhancement enables validators to engage with AVSs, requiring them to run supplementary software.

Concurrently, the EigenLayer smart contracts introduce new slashing conditions on the restaked Ethereum, predicated on the specifications of the chosen AVS. In exchange, these restakers are able to earn rewards for providing security to these systems. These conditions are agnostic to whether Ethereum is staked directly or via LSTs from an affiliated liquid staking provider. This makes it easier for distributed systems to build a security model without having to worry about bootstrapping security providers–stakers. Restakers can opt-in to multiple AVSs, exposing their stake to multiple slashing conditions and earning rewards from multiple AVSs. Ultimately, EigenLayer pools security through restaking instead of fragmenting it. Pooling security is what enables multiple parties to combine their resources to provide greater security for the entire restaking ecosystem.

Unveiling EigenLayer’s Potential: AVSs and New Yield Opportunities

The emergence of AVSs that can harness programmable trust heralds a transformative phase for distributed systems. Not only do they offer unprecedented access to inherited security, but they also unlock a myriad of additional yield opportunities for stakers. By providing security to these services, stakers can tap into innovative avenues for rewards while maintaining alignment with Ethereum’s long term goals and supporting the services they desire.

Potential Limitations of Restaking

Introduction to Potential Limitations

While restaking brings an enticing opportunity for stakers to amplify their returns, it's not devoid of challenges. The added slashing conditions introduced by platforms like EigenLayer lead to augmented rewards for stakers, compensating for the heightened risk. Yet, the architectural constraints of EigenLayer hint at potential composability issues with restaking positions, notably due to the intricate risk profiles that arise. This complexity mirrors the challenges that PoS grappled with during its early stages.

Future Scenarios for Restaking in DeFi

Broadly, there are two potential trajectories for the integration of restaking positions into the DeFi landscape:

Scenario 1: Governance-Gated Risk Management

Liquid staking providers might decide to mitigate some of the inherent risks of restaking strategies by implementing governance-based selections. Here, the strategies deemed appropriate for their users' risk tolerance are permitted. Consequently, this could lead providers to segment their offerings, targeting specific risk demographics. For instance, a platform like Lido, aspiring to be perceived as a 'safety-first' provider, may renounce users with a higher risk appetite, as they'll be more inclined to seek providers promising greater yields through aggressive restaking strategies.

Scenario 2: Non-Fungibility and the Push to LST Users

Should situations arise where dominant platforms like EigenLayer experience significant slashing events or there's a widespread erosion of trust in providers, it may become infeasible for liquid staking providers to endorse restaking at the node operator level. Instead, the decision-making may shift to LST users. Here, EigenLayer restaking positions could become the predominant staked asset representation. However, due to their distinctive risk profiles, these assets are inherently non-fungible. This poses challenges in assimilating them into the broader DeFi ecosystem since most protocols are parameterized based on price-based dependencies. Restaking positions would find trouble here due to their intrinsic scarcity of liquidity and limited price discovery.

The Conundrum of Staked Asset Financialization

While EigenLayer and similar platforms seek to fortify PoS networks through innovative staking models, the escalating complexities in validator risk profiles inadvertently spawn secondary challenges. Both aforementioned scenarios hint at a landscape where staked and restaked assets become fragmented and illiquid. This dynamic severely hampers the feasibility of leveraging restaking positions within the DeFi ecosystem.

Liquid Restaking Tokens (LRTs) Explored

Definition and Overview

Liquid Restaking Tokens, or LRTs, are the derivative representations of restaking positions. Analogous to LSTs, LRTs have emerged to grant broader and more intuitive access to restaking positions. Numerous protocols are championing this initiative, though the frontrunner is yet to emerge. Before delving into these protocols and distinguishing their attributes, it's essential to appraise the pros and cons of LRTs.

The Differences Between a Liquid Staking Provider and LRT Provider

Liquid staking providers and LRT providers have similar end goals, which is to provide stakers or restakers respectively with a liquid representation of their underlying position. However, they reach this end by different means. The liquid staking provider is solely focused on providing depositors with a means of connecting with a reliable node operator so that they can spin up validators and provide receipt tokens for staking positions. They help match capital to hardware operators. On the other hand, LRT providers must also account for the risk profile of AVSs which they opt-in to and further expose their LRT holders to. Liquid restaking helps manage capital delegation between yield opportunities as a form of portfolio management. Their goal is to return the user upside while minimizing risk exposure. Identifying an appropriate risk to reward framework which characterizes the LRT is one of the primary objectives of an LRT’s governance mechanism, whereas the governance mechanism for liquid staking providers is less objective.

Advantages of LRTs

LRTs facilitate more seamless integrations between restaking and DeFi. This aligns closely with the first potential future for restaked assets we previously discussed. That is, LST providers create liquid representations of restaking positions and manage them through governance-gating. This could enable LST providers to create well-defined risk profiles, enabling users to properly manage their portfolio of restaked assets and relish enhanced versatility. This approach enables restakers to participate in DeFi while still gaining the benefits of restaking.

Considerations for Users

While the benefits of LRTs are apparent, potential users should remain cognizant of their constraints. As described in the first scenario, many upcoming LRTs incorporate some form of governance oversight. This can restrict the flexibility of LRT holders to express their risk appetite and support their desired AVSs. This governance model raises pertinent questions about the motivations underpinning LRT providers' endorsements of specific AVSs and their ability to create a well justified risk to reward model. A transparent exploration of these motives in governance forums will be crucial for maintaining trust and transparency.

Challenges in Underwriting LRTs

The task of underwriting LRTs presents its own set of complexities. It might be equally, if not more, challenging than underwriting LSTs, given the nuanced risk profiles and unique pricing dynamics of LRTs. Addressing these challenges mandates protocols to adopt a more asset-specific approach towards creating markets for which LRTs can be sustainably supported. A deep understanding of the underlying mechanics of Ethereum core infrastructure, PoS, AVS design, and LRT design will be crucial. We’ll elucidate more on the design considerations for LRTs in detail in the subsequent sections.

LRT Case Studies

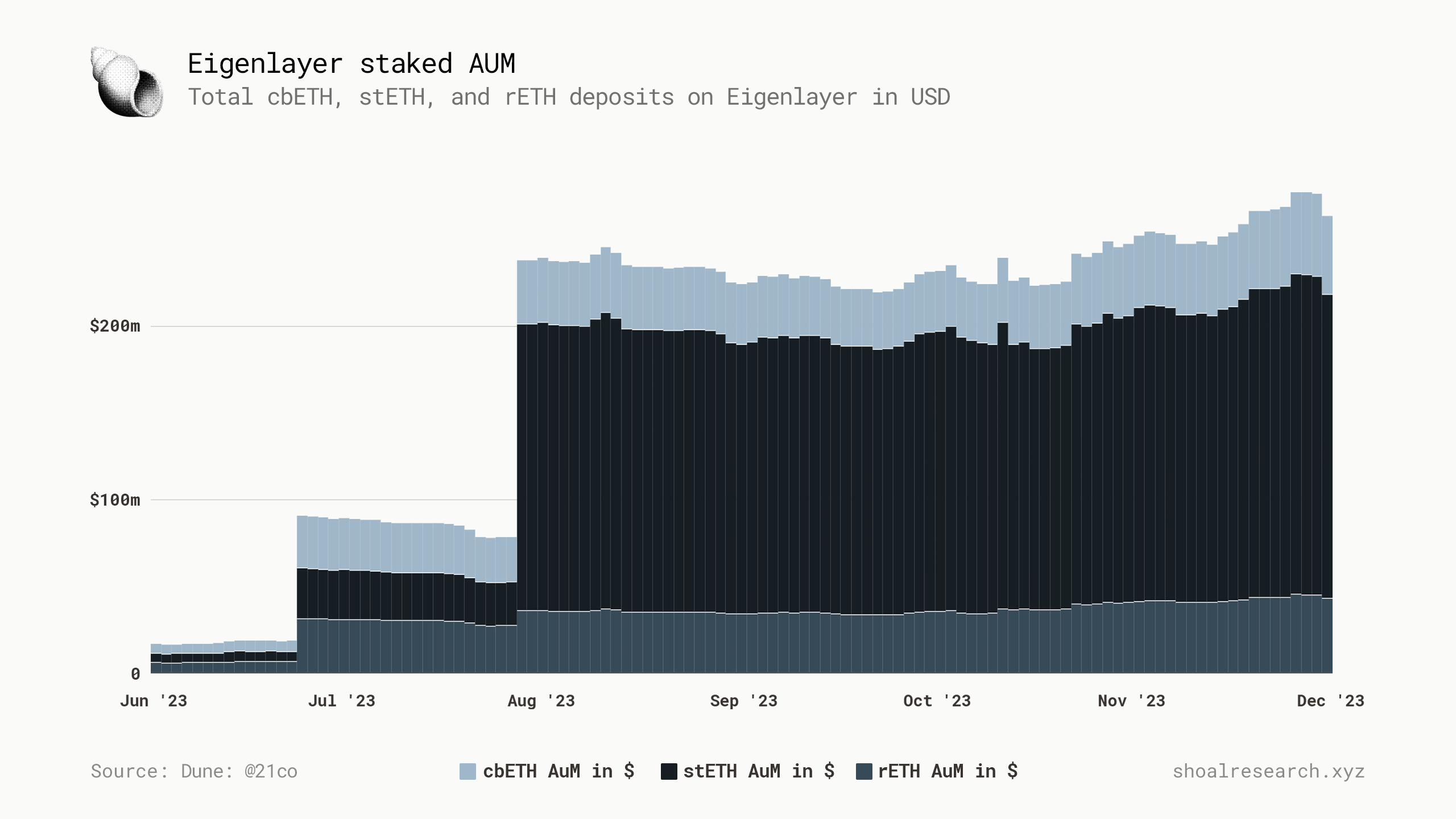

Now that we covered Eigenlayer, AVSs and the role of restaking, let's look at some case studies of early projects building in the ecosystem. As of now there are over 10 LRT projects building at the liquid restaking layer.

We dive deeper into the following projects:

KelpDAO (rsETH)

Renzo (ezETH)

EtherFi (eETH)

RestakeFi (rstETH)

Puffer (pufETH)

KelpDAO/ Stader (rsETH)

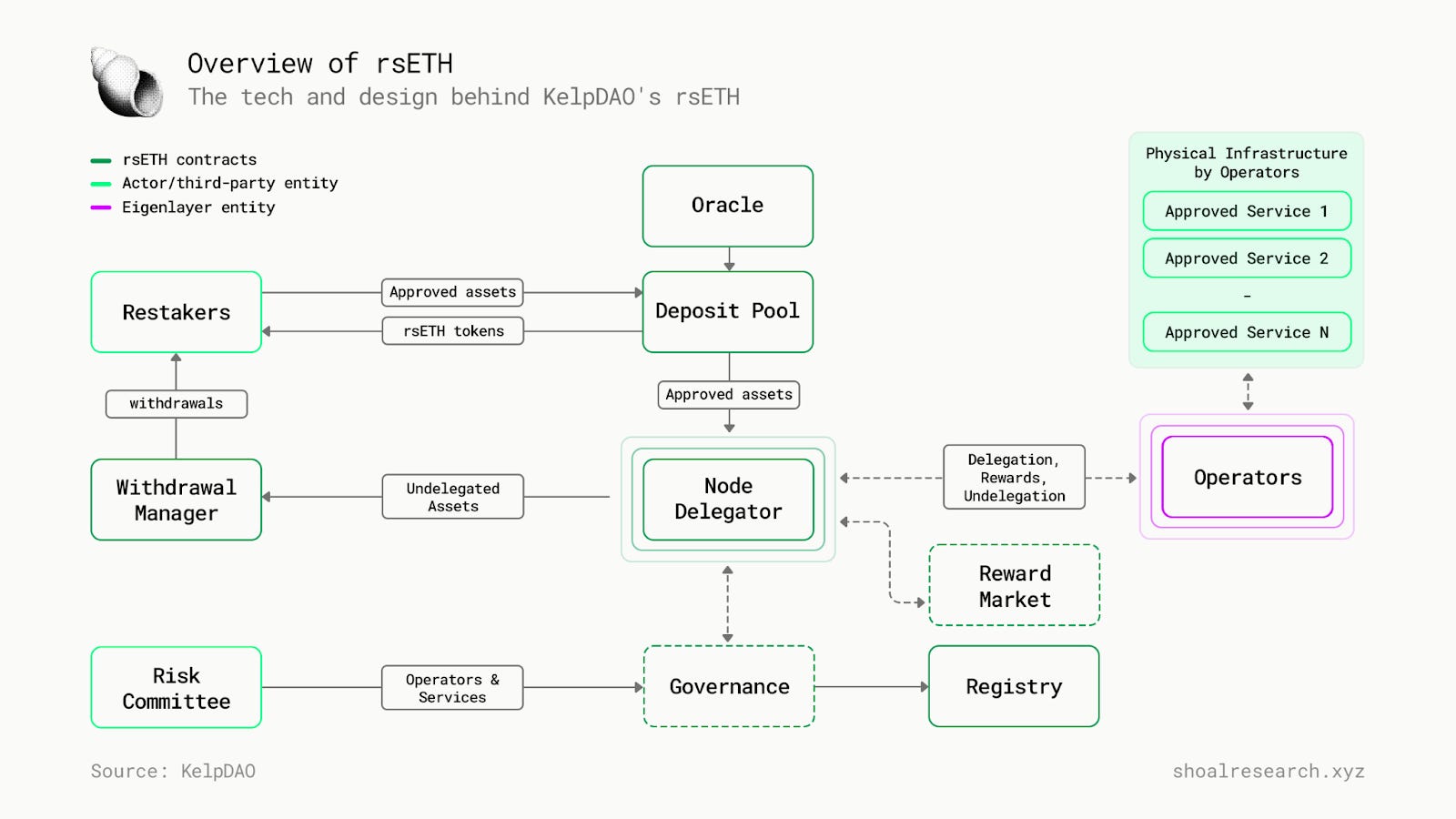

rsETH as a Part of Liquid Restaking

Fundamentally, an LRT, or Liquid Re-Staking Token, serves as a liquid representation of restaking positions to allow restakers on EigenLayer access to a form of their position that they can use in the greater DeFi ecosystem. RsETH is an LRT issued by KelpDAO aimed at addressing the risks and challengesposed by the current limitations of restaking position liquidity.

Restakers in Kelp engage by staking their LST to generate rsETH tokens, signifying partial ownership of a pool of the underlying restaked assets. Then, two rsETH contracts allocate the deposited tokens among different Node Operators collaborating with the Kelp DAO. Rewards accumulate from a diverse array of AVSs that were delegated to by the rsETH contracts. The value of the rsETH token reflects the underlying value of the various reward and staked tokens.

Restakers have the option to exchange their rsETH tokens for other tokens on AMMs for immediate liquidity or opt to redeem underlying assets through rsETH contracts. Restakers can further leverage their rsETH tokens in DeFi.

Isolated Architecture

The rsETH smart contracts are structured to segregate deposits, delegations, and withdrawals, ensuring a distinct division of responsibilities and minimizing the overall risk exposure to users of the protocol.

The overall structure includes 4 main modules: depositing and minting anLRT, moving assets to delegators, moving assets to strategies, and withdrawing. Depositing and minting rsETH automates the process of delegating to AVSs, saving the effort in identifying the right services and validators, and helping manage staking rewards.

Moving assets to delegators and strategies include transferring the tokens to Node Delegation Contracts (NDCs) based on tokenomics, weights, and distribution metrics. Strategies include delegating the funds from Node Delegator Contracts to Strategy Manager which distributes the funds among different strategies.

Upon a successful undelegation, the assets transition to NDCs, subsequently handed over to the Withdrawal Manager smart contract. The withdrawal manager determines the amount of assets to be allocated to the restaker based on the latest exchange rate. Once the funds are effectively withdrawn, rsETH is minted.

There are also 4 other modules supporting the Kelp DAO: registry (records operators, services, and assets in the rsETH ecosystem, including associated metadata and essential properties of rsETH), oracle (updates real-time asset prices for rsETH contracts, facilitating accurate minting and burning of rsETH based on deposit and redemption needs), governance (set of contracts that translate successful proposals into executable code to change smart contract behavior), and reward market (module optimizes non-ETH rewards through diverse extra-yield strategies, becoming a foundational layer for assessing and optimizing governance and utility tokens amidst the AVS surge).

Kelp x Stader

Amitej G and Dheeraj B, founders of Stader Labs, a multichain liquid staking platform with $230M+ in TVL, established Kelp DAO. The team is dedicated to developing Liquid Restaking Solutions for public blockchain networks.

Stader boasts more than 85,000 users and over $25 million in paid rewards, along with over 40 DeFi integrations. They have also forged partnerships with industry leaders such as Pantera Capital, Coinbase Ventures, Blockchain.com, Jump Capital, and other prominent funds in the space. Additionally, they have collaborated with renowned figures in the crypto world, including Sandeep Nailwal and Jaynti Kanani (Polygon’s co-founders), Nemil Dalal (Head of Crypto at Coinbase), Tim Ogilvie (Staked’s co-founder), and others.

Amitej and Dheeraj have successfully created one of the most robust liquid staking platforms across different chains, attracting significant capital and establishing partnerships with industry leaders. Their current commitment is to develop an LRT solution on EigenLayer for Ethereum.

The team has been diligently working on the design since Q1 2023 and was the first to publish the LRT intentions, coining the term LRT. Furthermore, the Kelp DAO has already undergone audits by some of the most trusted auditors in web3, including Sigma Prime and Code4arena, where no critical issues were found.

EtherFi (eETH)

EtherFi (eETH) is a decentralized, non-custodial Ethereum staking protocol that has evolved significantly since its inception. Initially, EtherFi focused on enabling a scalable network of solo stakers using Distributed Validator Technology (DVT). This technology divides validator keys, allowing a broader range of users to stake permissionlessly, addressing the requirement of having 32 ETH for staking and minimizing the centralization of slashing risk away from a single hardware operator.

In a more recent development, EtherFi has expanded into staking and liquid restaking verticals with their eETH LST/LRT hybrid. Here, users can mint eETH by staking ETH, which not only generates native ETH staking yield but is also natively restaked on Eigenlayer, thus enabling holders to receive double the staking rewards they earn from vanilla staking. This system differentiates itself from stETH (Lido) by eliminating the need for an additional restaking action on Eigenlayer, simplifying the process for users. Additionally, users will be able to further utilize their eETH in DeFi to earn additional yield if they wish to do so.

Mechanism Design

At the core of EtherFi's mechanism, ETH validators point their withdrawal addresses to Eigenpods. This setup allows users to earn Eigen points, which are expected to convert into protocol rewards later.

In the current landscape of EtherFi's staking mechanisms, it's crucial to understand that without Actively Validated Services (AVS) being live, a Liquid Restaking Token (LRT) effectively operates in a manner akin to a Liquid Staking Token (LST). However, with the future activation of AVSs, it is expected that LRTs will yield relatively higher rewards, though they may also bring increased risks from additional slashing conditions.

Renzo (ezETH)

Renzo (ezETH) is an LRT platform and Strategy Manager for Eigenlayer. It is built to serve as an interface for Eigenlayer, abstracting away many of the technical, financial, and risk management barriers for market participants and enabling easier access to the emerging restaking primitive. The same way Eigenlayer enables any distributed system to inherit Ethereum’s security, Renzo enables any on-chain user to help secure the networks being built on top of this new primitive–AVSs. Renzo helps bridge the gap between the AVSs which need security, and users who are attempting to balance the risks and rewards of restaking.

Mechanism Design

Users can deposit either ETH or any supported LST (stETH, rETH, cbETH) on Renzo to mint an equivalent amount in ezETH. For every 1 ETH/LST deposited, 1 ezETH is minted.

Formally the value flow runs from ETH Staking → Eigenlayer AVSs → Renzo Restaking. By securing Eigenlayer AVSs, Renzo offers a higher yield than vanilla staking and is thus expected to drive more volume and participation to ETH staking as a whole.

ezETH is a yield-bearing asset which works similar to Compounds cTokens, where the value of ezETH reflects the restaking rewards earned on the underlying position; generally the price of ezETH increases relative to its underlying LSTs as the position accumulates rewards earned in AVS tokens. Rewards are distributed in ETH, USDC, and AVS tokens.

The core function of Renzo is to help secure Eigenlayer AVSs, and the protocol offers restaking strategies where users can decide to secure one or more networks to earn yield. As each AVS represents a unique entry for rewards (as well as risk), the restaking ecosystem will supposedly benefit from a greater number of AVSs, as this brings in more diverse strategies for restakers.

This opens up the doors for new opportunities for protocols and services to be built and implemented; ecosystem-native LRTs which secure a specific AVS and offer holders unique opportunities such as priority execution and fee rebates, financial primitives such as risk/reward management strategies for LRT holders, dual-staking marketplaces, and more. Furthermore, upon launch, any team will be able to permissionlessly build the restaking infrastructure end-to-end to benefit from the restaking ecosystem while controlling the entire flow with or without a token, enabling teams to custom-build infrastructure to meet their specific preferences in a flexible manner.

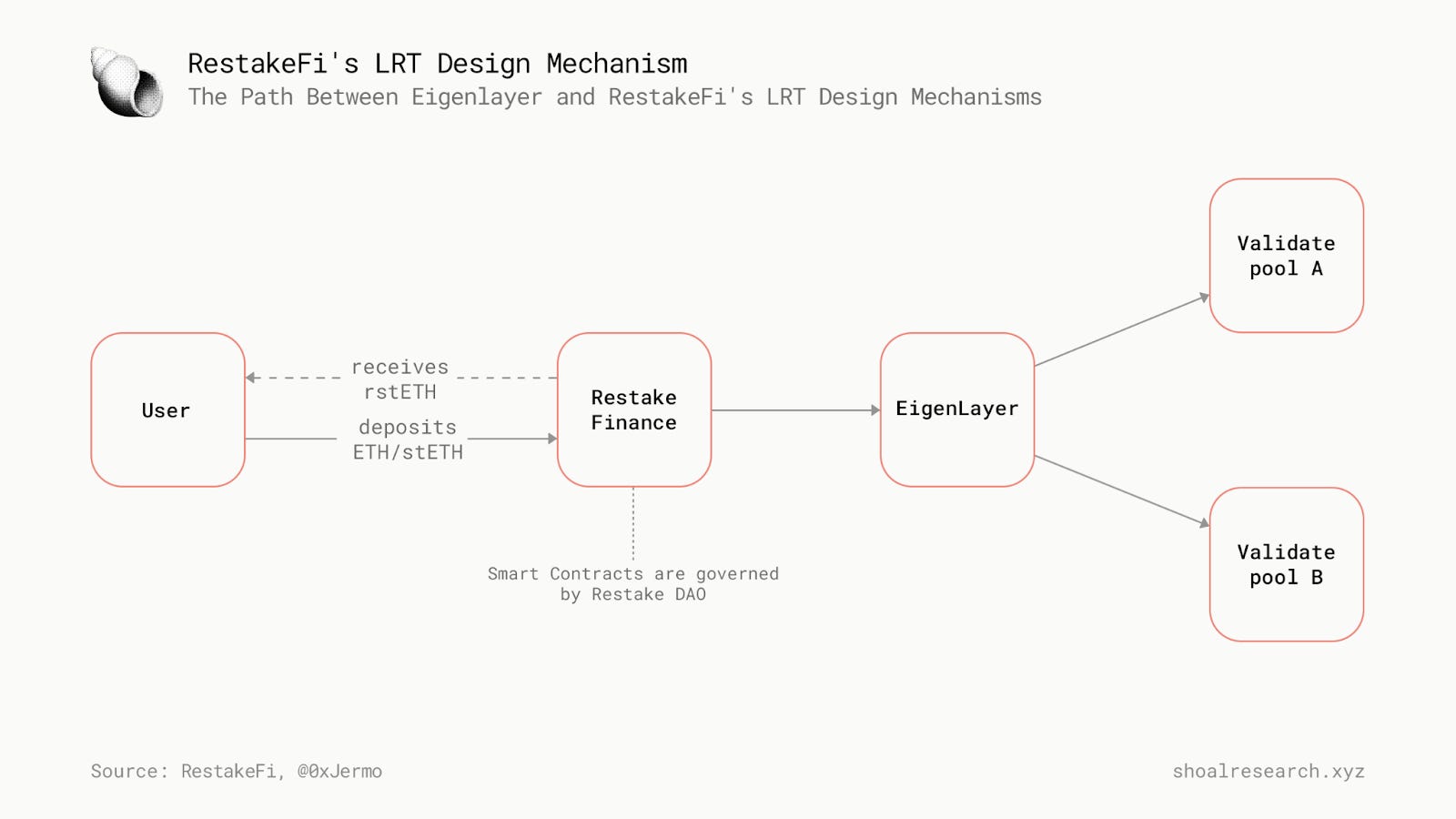

RestakeFi

Restake Finance refers to itself as 'the first modular liquid staking protocol for EigenLayer. A user will be able to deposit their ETH or stETH in EigenLayer via smart contracts governed by the Restake Finance DAO. In turn, depositors will receive rstETH, which incorporates a rebasing and yield-bearing mechanism. Re-basing will occur on a daily basis, resulting in an increase in rstETH in your wallet. Please note that this does not include the yield earned from EigenLayer; that requires a separate claiming mechanism.

The unique mechanism behind Restake is that depositors will eventually be able to choose the modules they want to validate. A user has the option to validate as many (or as few) pods as they prefer. A risk-averse user will likely opt for a single pod with an established team and track record, while a user with a higher risk appetite may seek more yield and, consequently, choose to validate more pods.

Puffer (pufETH)

Puffer Finance aims to stimulate validator decentralization through a network of homestake nodes by reducing the initial amount from 32 ETH to 2 ETH. This is made possible by a novel remote signing tool known as ‘Secure-Signer,’ which aims to prevent slashing risks while utilizing Trusted Execution Environments (TEEs) such as Intel SGX. The Secure-Signer tool manages validator keys on behalf of the consensus client and can be run locally or remotely. When running within a TEE, it secures the validator keys using applied encryption when the keys are at rest, ensuring they cannot be used otherwise.

In addition to the TEE, validators also benefit from having their keys secured within it. Puffer is unique in that it can support Application-Specific Validators (ASVs) that require some form of privacy, such as privacy-preserving Layer 2s.

To actively participate in the validation set of a designated ASV, a staker (referred to as a Puffer) can deposit any amount over 0.01 ETH, which is added to a pool of ETH. This pool serves as a reserve that can be tapped into to form a new node for validators. This ETH will be staked if the requirements (32 ETH per node) are fulfilled, and in return, a Puffer will receive pufETH, a yield-bearing token similar to Compound’s cToken structure, which increases in value over time due to the accrual of rewards.

To redeem their underlying ETH, Puffers can burn their pufETH, receiving the original ETH and accrued rewards if there is sufficient liquidity in the withdrawal pool. To facilitate this, a portion of all deposited ETH into Puffer Finance, as well as rewards and node withdrawals, is added to the withdrawal pool to provide exit liquidity.

Conclusion

In this piece, we’ve explored the evolution of Ethereum’s consensus mechanisms (both past and present), focusing on the transition from PoW to PoS, and the innovative development of LSTs and LRTs. Ethereum’s Merge introduced PoS to the network, which marked a significant shift towards more sustainable and scalable blockchain security. LSTs emerged as the solution to the liquidity challenges stakers originally faced, allowing users to participate in DeFi while staking. The LRT further builds upon this, offering enhanced yield opportunities and security contributions for users participating in Eigenlayer’s restaking ecosystem.

The benefits of LRTs are not without their risks. This research covered the most pertinent risks to LRT holders such as composability, the potential for slashing, and the complexities that arise in the management of restaking positions and their risk profiles (i.e. what AVSs they opt-in to and why). We also highlight the innovations in the space, including projects like EigenLayer – the pioneers of restaking – and platforms like KelpDAO and Puffer Finance that aim to democratize access to restaking via their LRT solutions.

Overall, the piece provides a comprehensive analysis of the current state and potential future of Ethereum's consensus mechanisms, highlighting both the opportunities and challenges in this rapidly evolving landscape. The integration of restaking into Ethereum's ecosystem represents a significant milestone, offering a more sustainable and scalable approach to blockchain security and opening up new avenues for yield generation in the DeFi space.

Sources

Investment Disclosure. Disclosure: Members of Shoal Research hold material positions in the assets discussed in this article. The content presented is for informational purposes only and should not be construed as financial or investment advice. Please perform your own due diligence before making any investment decisions.

Not financial or tax advice. The purpose of this newsletter is purely educational and should not be considered as investment advice, legal advice, a request to buy or sell any assets, or a suggestion to make any financial decisions. It is not a substitute for tax advice. Please consult with your accountant and conduct your own research.

Disclosure. All of my posts are the authors own, not the views of their employer.

Now that's what I call good research.

Strong analysis 💪🏽