The Convergence of Yields

The intersection and influence of traditional finance on DeFi yields

“Show me the Incentives and I’ll show you the outcome” - Charlie Munger

This simple yet profound phrase by Munger, like every good quote, encapsulates rational human behavior in a few words. In many situations, incentives might be subtle or too complex to perceive, but in finance, it's often more straightforward — people want to maximize their profits and minimize their losses.

Decentralized Finance — DeFi — cuts out the middlemen, simplifying the link between incentives and outcomes. Seeing assets moving from protocol to protocol, fresh money coming in, and money coming out is like seeing human behavior at its rawest and clearest form: when there's a clear reward, people act. This clarity around rewards, the low barrier of entry, and, of course, the promise of a high yield is what's driven DeFi's rapid growth.

In these unpredictable economic times, with rising inflation, soaring interest rates to tackle that very inflation, and consequently more attractive low-risk bonds, it's crucial to understand where DeFi stands and its response to these challenges.

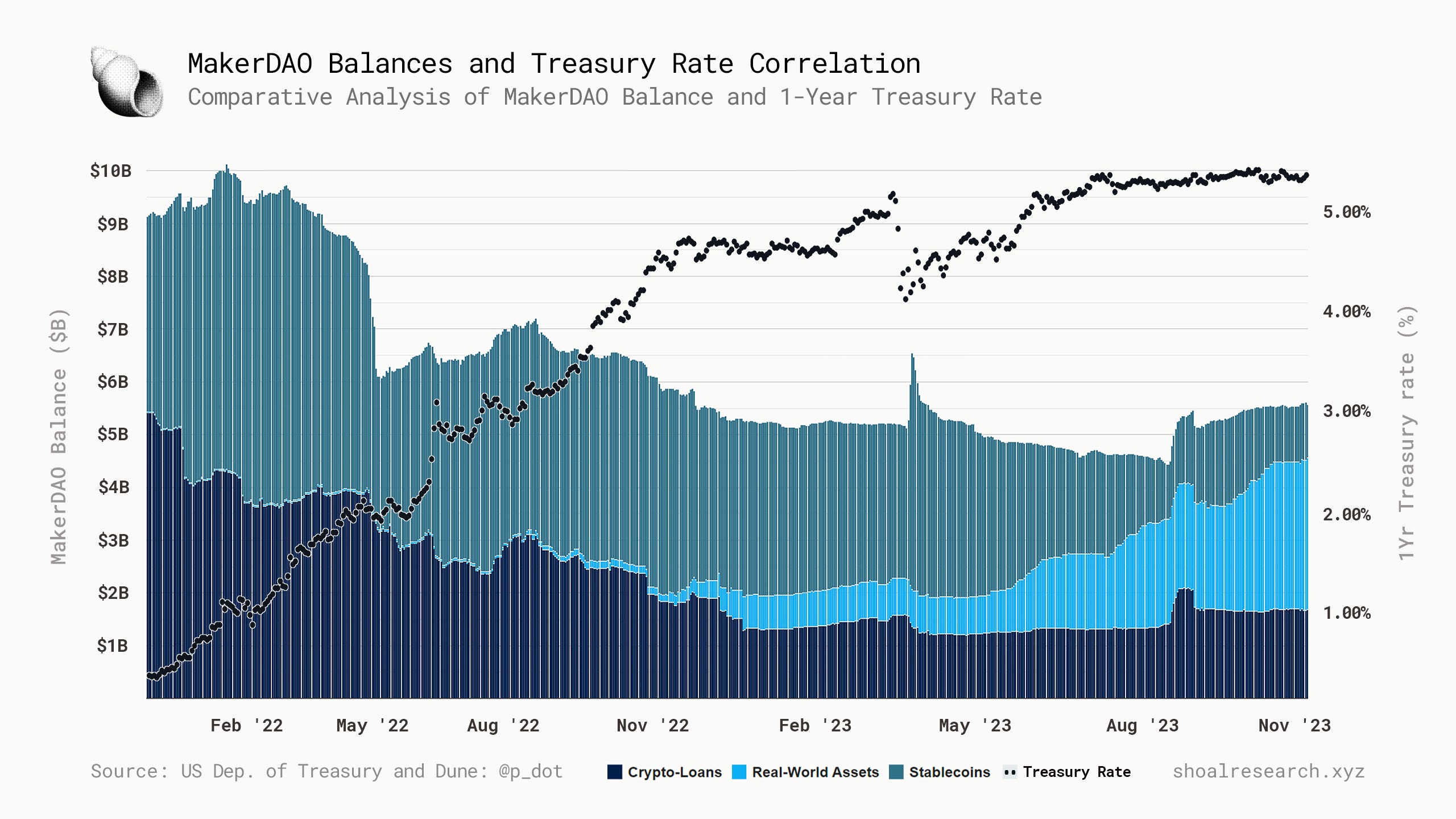

MakerDAO’s high revenue coming from RWAs (increasingly influenced by the US bond rates), combined by its current dominance in the stablecoin money market is allowing MakerDAO to essentially act as the DeFi (De)Central Bank and to determine the base DeFi rate for money markets.

In this blurry scenario, we'll also shed light on the necessity of increasing the variety of on-chain native forms of yield, that don’t exclusively depend on volatility or traditional financial cycles.

Different Sources of Stablecoin Yield in DeFi

In DeFi, when individuals hold a stablecoin, they essentially have three options:

Keep it idle (which is not ideal because the US dollar suffers from an inflationary process and the stablecoin is worth less every day);

Find a strategy to get a yield on top of this stablecoin; or

Swap its stablecoin for another token and strategy in DeFi (which, in this article, we'll simplify as buying ETH and staking it).

Assuming investors choose to hold their stablecoins to maximize returns and offset inflationary losses, they have several strategies at their disposal:

Staking: Locking up your token to support a network and earn rewards, like interest on a savings account but with network validation perks. Or simply deposit it in a smart contract (in the case of stables or other DeFi strategies).

Market Making: Providing liquidity to decentralized exchanges — DEXs — for smoother trades, earning some of the trading fees.

Lending Platforms: Lending your assets on smart contracts to earn interest, a decentralized money market with its own set of risks.

Tokenized Real-World Assets: Keep your money on-chain and gain exposure to TradFi investments, like bonds, for example.

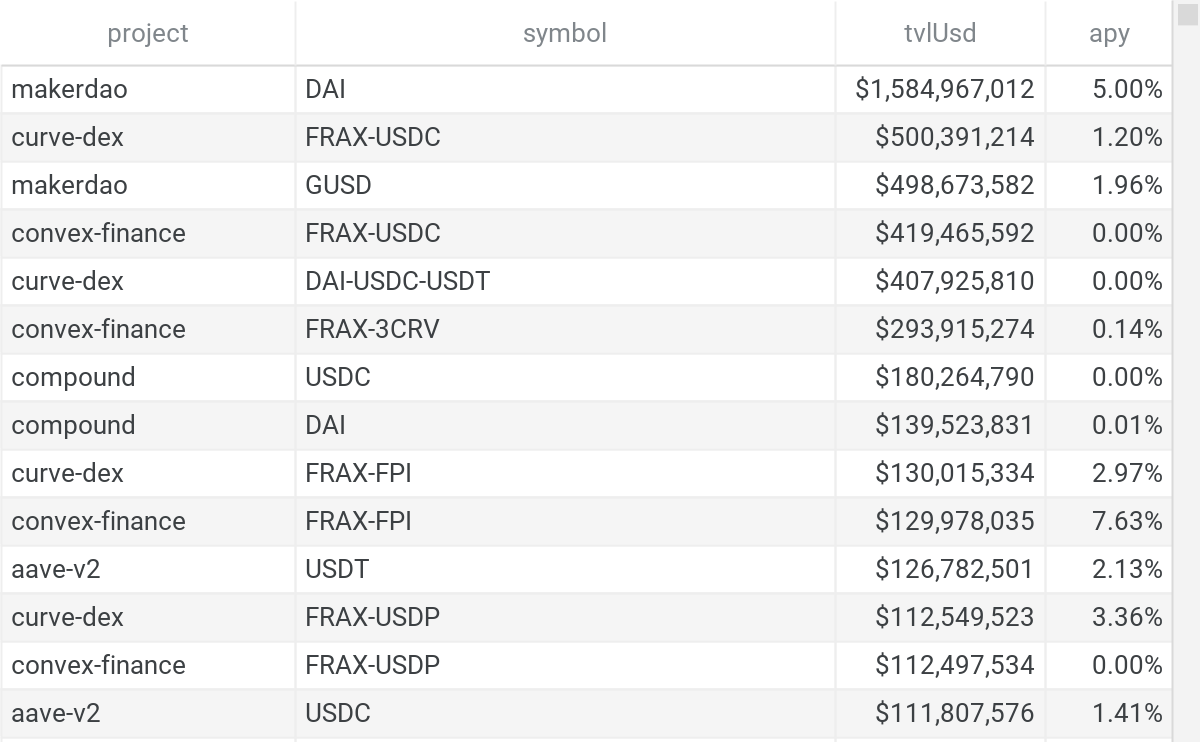

To understand how investors currently allocate their stables in smart contracts, we’ve prepared Table 1, which outlines all those different sources of yields on the Ethereum mainnet. The columns depict the following:

The project behind a certain strategy;

The symbol (tick) of the tokens used in the strategy.

The Total Value Locked (TVL) indicates the aggregate amount (in dollar terms) invested in the strategy.

The Annual Percentage Yield (APY) denotes the expected yearly return.

The first thing that gets our attention when analyzing the data of this table is how dominant MakerDAO’s DAI (DSR) strategy is, with an APY of 5% and 1.6 billion dollars deposited in its contracts. It represents a staggering 52% of the sum of the entire market other than this strategy represented by this table. The Dai Savings Rate (DSR) within the MakerDAO ecosystem allows DAI stablecoin holders to earn interest on their DAI through a combination of off-chain and on-chain yield strategies, including ETH staking and treasury yields.

But it has not always been like this.

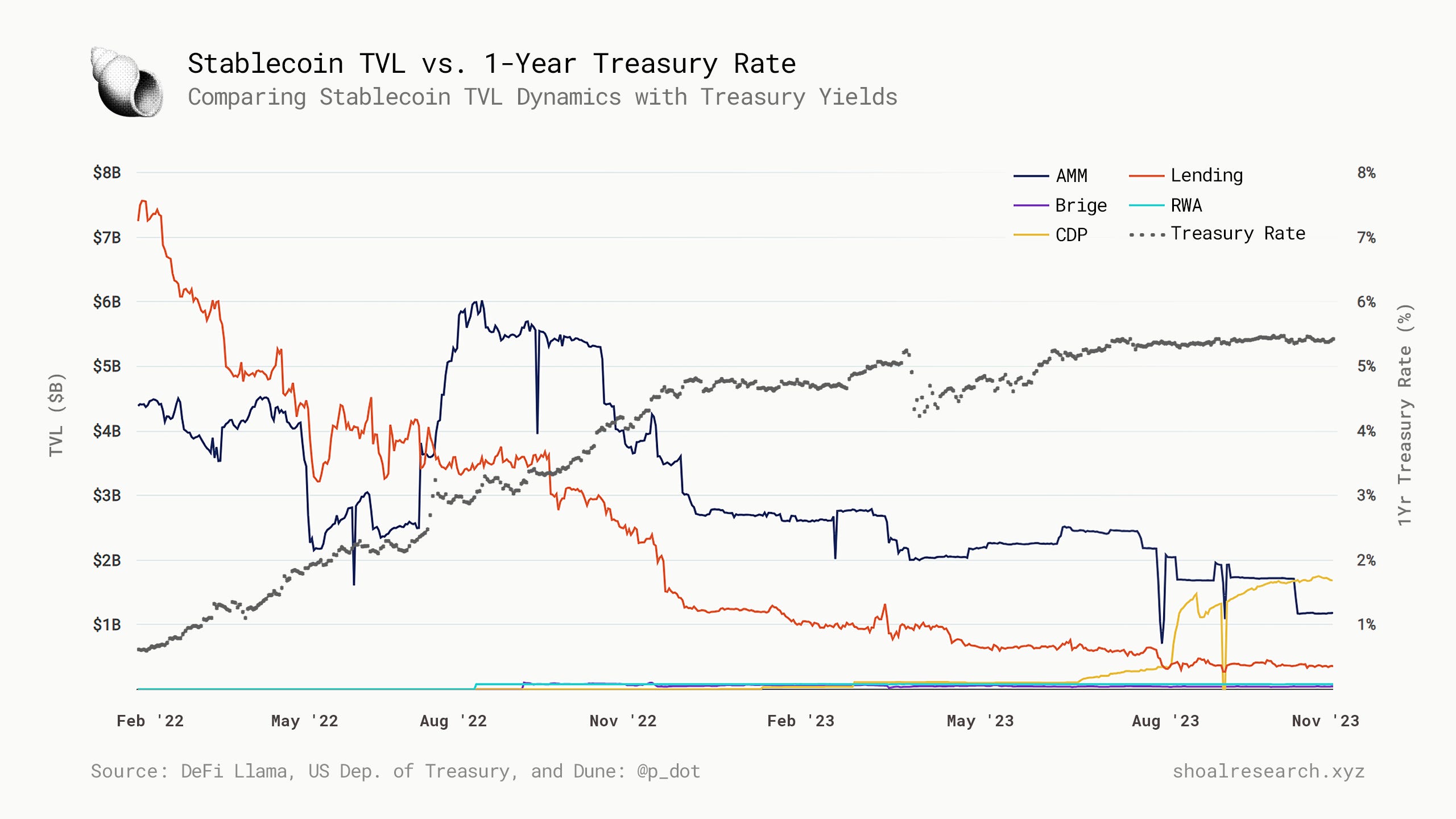

Dai Savings Rate — DSR — TVL has been growing rapidly, especially since August 2023. In Chart 1, we can visualize the TVL by type of yield strategy and how they have changed in the past year. We can see how the AMM and Lending TVLs have significantly declined in that time.

Chart 2 makes it more clear how the total TVL of the studied protocols has ranged from 3 to 4 billion dollars and how there is a significant change in the composition of the aggregate TVL, with collateralized debt positions, referred to as CDPs (DSR) gaining a substantial part of it. CDPs function as decentralized financial instruments that are secured through the on-chain pledging of other assets. In this study, the DSR is a CDP backed by a combination of on-chain and off-chain assets.

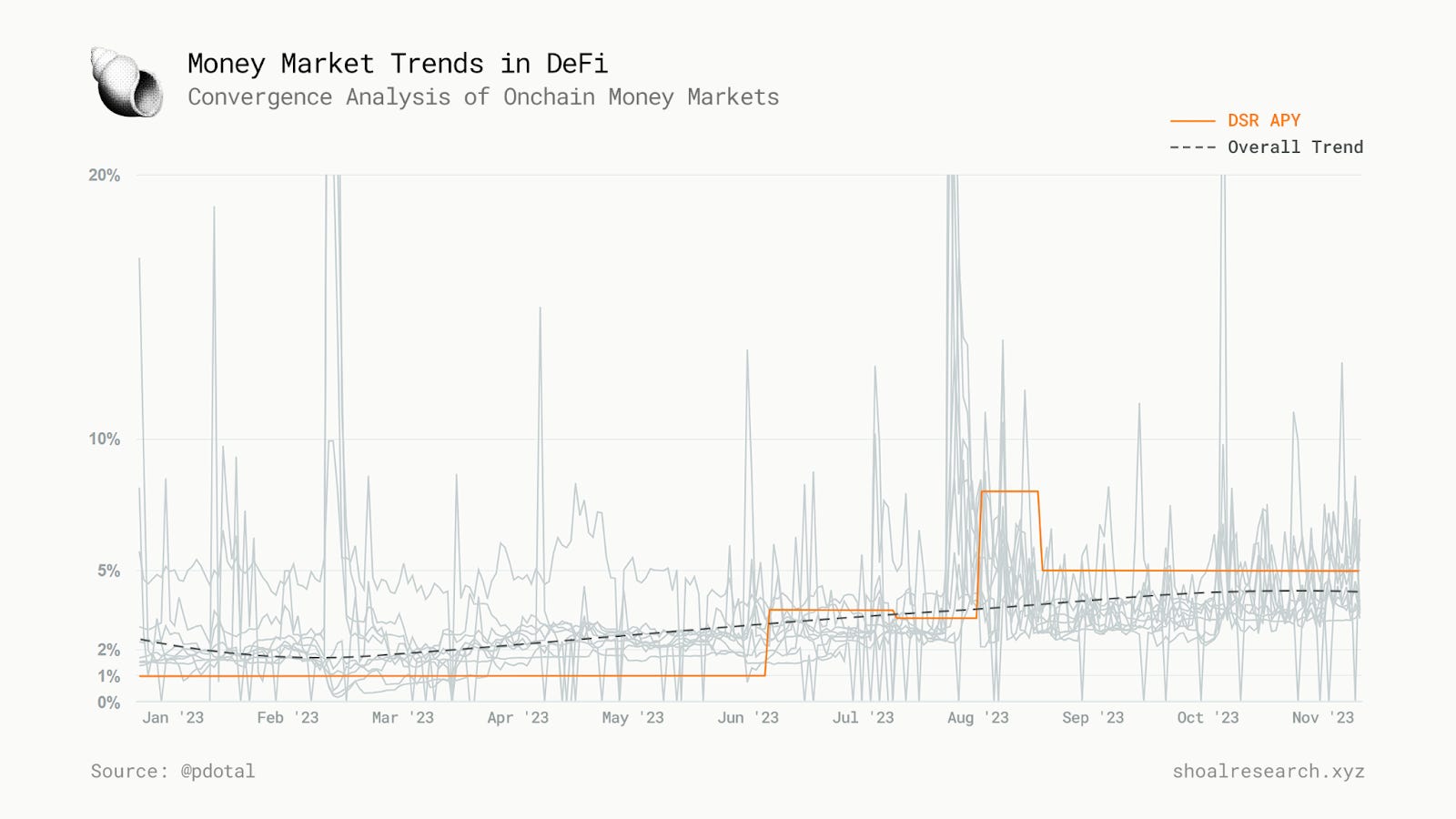

It is clear that something is happening for this composition change to occur. Still, to understand the behind the scenes of this phenomenon, it is crucial to understand the behavior of the yields of the money market and how they have reacted to DSR. Chart 3 describes this.

The APYs of different money markets (minus DSR APY) on the Ethereum mainnet are represented on the chart. The plot is composed of three sections separated by colors, divided by two events (dotted lines): the hikes of the Dai Savings Rate on June 19th and August 6th.

The Overall Trend represented by the dotted blue line makes it more evident what is happening. The APY trend of all other money market protocols has doubled; investors seem to have removed their positions from money markets and invested it somewhere else (probably DSR), until it reached a new equilibrium. It looks like DSR is dictating the rates, and the money market is converging with the DSR.

But why exactly is this happening?

The Ideal of Convergence

Before diving deeper into why these rates converge at a new equilibrium dictated by DSR, it is important to understand the ideal of convergence.

Theoretical Fundamentals of Yield Convergence in a Perfect Market

In economic literature, the Law of One Price posits that in a frictionless and perfectly competitive market, identical goods or assets will have the same price. Extending this to DeFi (and yields), in a perfect market scenario, yields across various asset categories (like stablecoins) and protocols should converge to a single rate. This is because, in such a market, all participants have access to the same information and can move assets freely without any barriers, leading to a single equilibrium yield.

The Role of Arbitrage in Pushing Rates Towards Convergence

Arbitrage plays a pivotal role in driving the convergence of yields. When there's a discrepancy in yields between two similar assets or platforms, informed investors can move their funds from the strategy, paying lower yields, and deposit in the one with the higher yield. This movement naturally pushes the yields of the two assets closer together until the opportunity for yield arbitrage diminishes. The continual pursuit of these arbitrage opportunities by market participants helps keep the yields in check and drives them toward convergence.

Factors Preventing Perfect Convergence

While the theory sounds neat, real markets are not that perfect. Several factors can prevent yields from perfectly converging:

Information Asymmetry: Not all market participants have access to the same information at the same time.

Gas fees: Moving assets between protocols or swapping one asset to another often involves fees, which can deter arbitrage.

Regulatory Barriers: Different regulatory environments across regions can restrict the movement of assets or the participation of certain investors (lending, providing liquidity, and staking can be taxed differently, for example).

Risk Differentials: Even if two stables may represent the same denomination, they might, by default, have different underlying risks. And strategies involving them might have other risks on top of that, leading to different yields.

With the theory being clear, let’s understand the events that have happened and have been happening that are shaping the DeFi stablecoin market the way it is today.

Major Events of Convergence

The most important factor that permeates the changes happening in DeFi and this convergence event is the interest rate hikes performed by the FED in the US to control the high inflation.

This high-interest rate environment hinders economic activity, investment, and high-risk investment, among other factors, because it creates a high opportunity cost for doing anything else. There’s a high paying government bond with low risk, producing the same yield or even more than DeFi protocols.

It can be clearly seen on Chart 4 how the Lending and AMM markets were affected. But what gets our attention is how Maker DAO’s DSR was able to increase its TVL to such a significant level in such a short time, in the worst market circumstances.

Chart 5 gives us the biggest response to the underlying events we’re exploring: MakerDAO has been increasing its allocation on RWAs, which provide direct exposure to traditional finance and its current high-interest rates. This was a move by the DAO to get exposure to these high rates at a low risk with their vast stablecoin reserves, allocating more and more assets into RWAs to surf this high-interest rate environment. So much so that now it represents 52% of the entire balance sheet of the DAO.

Because of this allocation, currently, 66% of the revenue from the DAO comes from RWAs, and 30% comes from ETH liquid staking. This movement encapsulates the reaction of DeFi as a whole to the high-interest rates environment.

MakerDAO’s high revenue coming from RWAs (directly influenced by the US bond rates), combined by its current dominance in the stablecoin money market is allowing MakerDAO to essentially act as the DeFi (De)Central Bank and to determine the base DeFi rate for money markets.

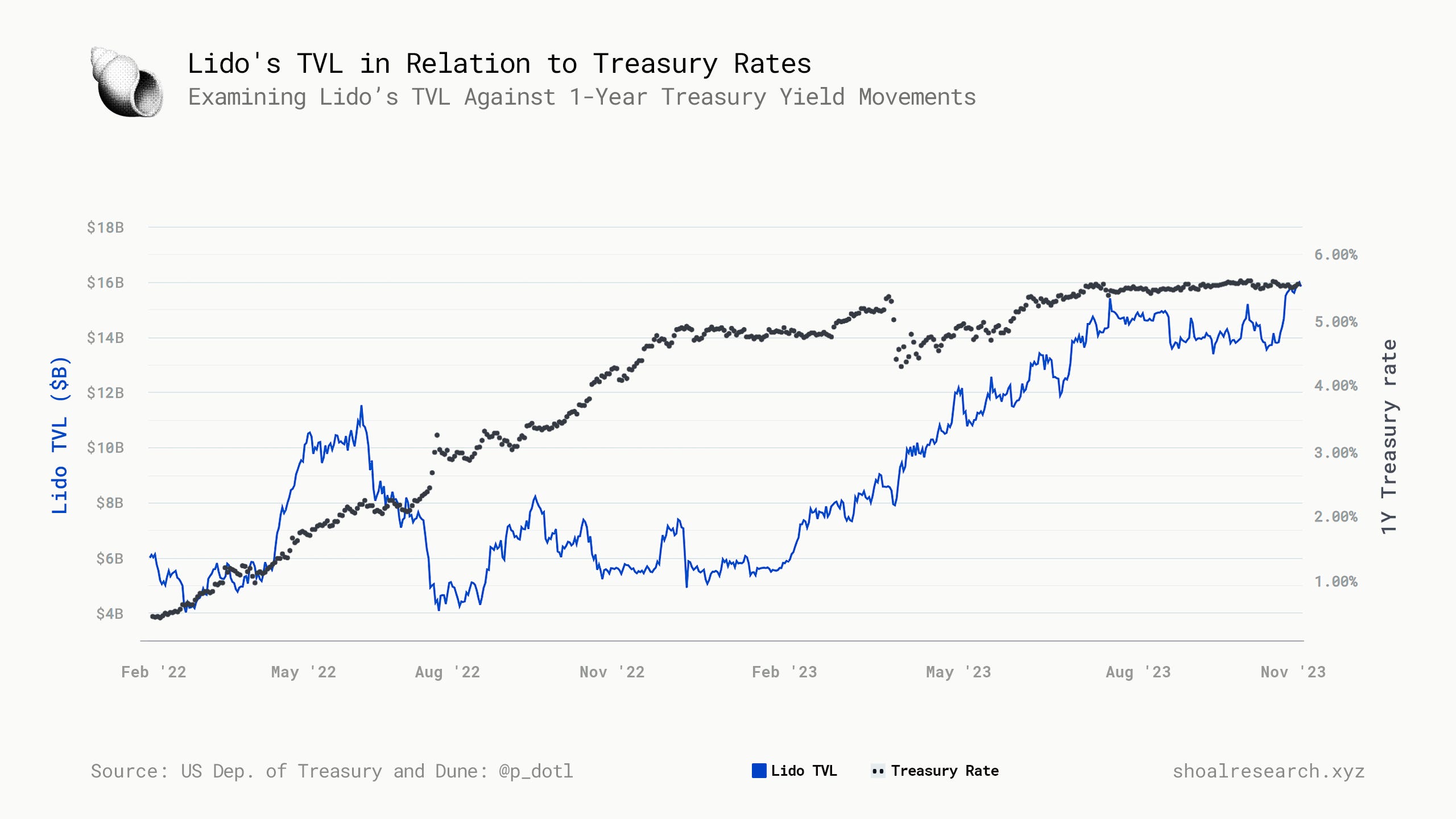

The significant revenue coming from ETH also gets a lot of our attention. Despite the interest rates going up, and consequently, DeFi TVL going down as a whole, staked ETH TVL was shooting up. Staking ETH became an alternative for those looking for a safe yield. ETH staking yield became blockchain’s de facto ‘risk-free’ rate.

These interesting events come at a price — ultimately, this convergence is the convergence of stable yields in DeFi, through RWAs, with rates in traditional finance. In this environment, where stable yield from DeFi money market solutions is not as eye-catching as TradFi yield, even fully on-chain stables like DAI became increasingly integrated with the risks of Traditional Finance.

This opens up a significant opportunity for crypto-native stable yield solutions that aligns more closely with the web3 market and less with traditional finance. The challenge lies in its ability to offer competitive yields against TradFi, even during economic downturns, and low volatility without necessarily mirroring its behavior.

Time for On-chain native yields

There is evident demand for yields less correlated with the real-world economy, it just has to offer attractive returns even in the case of economic downturn. Web3 requires yield sources that are more closely aligned with its own dynamics and less susceptible to the disruptions, risks, and censorship prevalent in traditional finance.

This task isn't easy. Traditional finance, developed over centuries, is deeply rooted in path dependence. It has adapted to numerous regulations and incurred significant sunken costs, making it hard to move away from these established models to create something new. Yet, the beauty of building DeFi lies exactly in overcoming this challenge.

Builders have the golden opportunity to improve the current system, adapting it for a world of sovereign individuals. There's unlimited opportunity to build something new, leveraging the innate characteristics of this new world, free from the constraints of inefficient regulation and control.

We welcome innovation in new yield sources, fostering native financial cycles in DeFi. This involves capital flowing between convergence and divergence cycles with native and traditional yield sources on-chain, with the freedom of capital movement, aiming to create a unique environment of financial freedom, driving finance and freedom forward.

Conclusion

Over the past year, the stablecoin market has faced significant changes, with a clear shift in TVL composition and a convergence of yields, spearheaded by the Dai Savings Rate (DSR) and its reliance on Real World Assets (RWAs). This trend has introduced a level of risk to the stablecoin market as yields became increasingly dependent on TradFi and its associated risks.

As stablecoin yields start to reflect traditional financial markets more closely, the line between DeFi and TradFi begins to blur. This shift may challenge the core principles of decentralization and autonomy that DeFi represents, as it becomes subject to the same economic pressures that affect the broader financial world.

In this context, the introduction of new web3 native sources of yield is necessary to create a more dynamic market where on-chain cycles are not solely dependent on the volatility of the market or traditional finance. The future of DeFi depends on different on-chain cycles that allow capital to move freely inside our own ecosystem and break away from the rusty shackles of control and traditional finance.

You can find more about Pedro on Twitter

Sources

Investment Disclosure. Disclosure: Members of Shoal Research hold material positions in the assets discussed in this article. The content presented is for informational purposes only and should not be construed as financial or investment advice. Please perform your own due diligence before making any investment decisions.

Not financial or tax advice. The purpose of this newsletter is purely educational and should not be considered as investment advice, legal advice, a request to buy or sell any assets, or a suggestion to make any financial decisions. It is not a substitute for tax advice. Please consult with your accountant and conduct your own research.

Disclosure. All of my posts are the authors own, not the views of their employer.

| A guest post by

|