Uniswap v4: The liquidity Marketplace

Understanding uniswap v4 and its shift to a liquidity platform

Shoal Research Contributors: Gabe Tramble

Preface

Uniswap, the ERC-20 AMM, has played a pivotal role in revolutionizing decentralized finance (DeFi) through its successive versions. Uniswap v1 allowed users to swap ETH to ERC-20 tokens, while v2 allowed users to trade ERC20 tokens with other ERC20s. V2 also added a wide range of assets that were not yet available on any other exchanges, all using a constant product market maker (CPMM) model. The constant product market-making model, X*Y=K, allows users to trade with a pool of tokens rather than with direct peers or market makers. The revolutionary Uniswap v3 allowed liquidity providers the freedom to concentrate their liquidy range in a liquidity position (LP), which improved capital efficiency but added complexity and increased gas costs for users.

Capital efficiency: “Effective utilization of resources to generate maximum output or returns. Prevention of idle money.” - Shoal Research

Each version pushed the capabilities of decentralized exchanges, empowering users and driving innovation in the DeFi space. With the upcoming release of Uniswap v4, the protocol is set to introduce even greater customization and flexibility through hooks, further solidifying its position as a leading decentralized exchange platform. This article explores the features and enhancements of Uniswap v4. Let's walk through the v4's architecture and uncover how they plan to improve the DEX landscape.

Uniswap v3, Concentrated Liquidity

Before diving into the specifics of v4, it is crucial to understand Uniswap v3, a landmark development in the AMM landscape. V3 introduced concentrated liquidity, an innovation that allows liquidity providers to designate specific price ranges for their capital. By providing specific price ranges for liquidity, LPs can earn greater fees boosting capital efficiency. Uniswap v2 is based on the constant product formula X*Y=K, which at the time was novel because it created markets for illiquid assets. However, has reduced capital efficiency since liquidity was spread infinitely along the liquidity curve. Meaning whenever an LP provided liquidity, they supported all asset prices.

With the advent of v3, users were given more autonomy to specify fee tiers and even liquidity ranges, leading to higher capital efficiency and deeper liquidity.

Uniswap v4, AMM Marketplace

Taking v3 a step further, Uniswap v4 introduces new customization through the Singleton contract and hooks, which we will detail shortly. These innovative solutions aim to streamline on-chain computations, reducing costs and some complexities while offering more capital efficiency and flexibility with protocol designs built on Uniwap. Before v4, Uniswap v3 assigned core immutable parameters that the core team calls "opinions," such as fee tier and other predefined structures, meaning the Uniswap team came up with immutable features for v3 that are now customizable in v4. With v4, developers can become "expressive" about the liquidity pool parameters, which is expected to lead to extensive financial primitives on top of the Uniswap liquidity layer.

Liquidity Platform

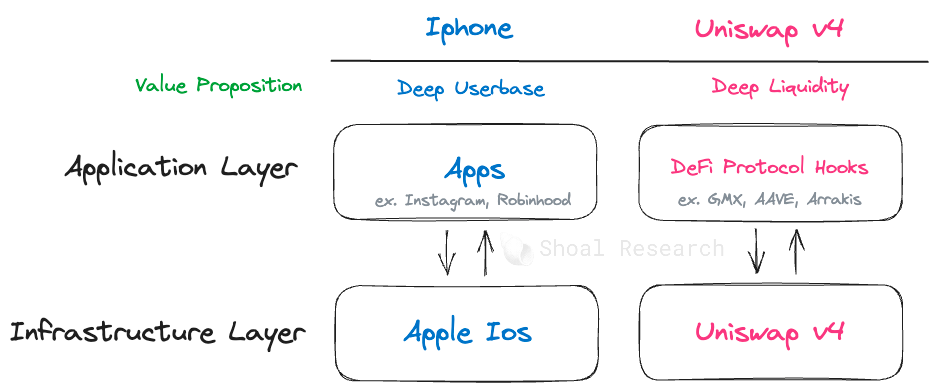

Lack of liquidity is one of the core issues in the DeFi space, as protocols need substantial liquidity to perform extensive DeFi operations. Uniswap v4 aims to serve as the liquidity layer for many of these protocols.

Think of Uniswap v4 with regard to the iPhone ecosystem. Apps like Telegram, Twitter, and Instagram are developed and deployed to the Apple App Store, reaching an extensive user base. Similarly, liquidity management protocols, DEXs, and other Dapps can tap into Uniswap V4 to utilize its liquidity through hooks. Just as users visit the App Store to obtain desired apps, users can turn to protocols built on Uniswap V4 to access the specific liquidity strategies and other tools they desire.

By leveraging a platform-based approach, Uniswap v4 can benefit from network effects by other protocols developing on its liquidity layer. Network effects are a phenomenon particularly observable in social media, which refers to the exponential growth of products as they accumulate more users, eventually leading to a dominant market position.

What exactly is the Singleton contract?

The singleton contract structure is an innovative feature of Uniswap v4 that consolidates multiple token pool contracts into one overarching contract. In the example below, for an ETH/DAI swap, the trade routes between multiple trading pair pools to reach the desired outcome. With the singleton contract, the trade is routed through one contract full of many trading pairs. Instead of moving tokens between pools, the contract does balance accounting similar to swaps on centralized exchanges, known as Flash accounting.

Flash Accounting

Flash accounting updates the internal net balance and executes external transfers only at the end of a block, reducing gas costs while simplifying complex pool operations like atomic swapping and liquidity addition. Flash accounting also enhances the efficiency of multi-hop trades, delivering cheaper costs for swapping and improved slippage on multi-hop swaps. This innovation benefits end users by making transactions more affordable and seamless.

Combining the singleton contract and flash accounting, Uniswap founder Hayden Adams estimates a 99% fee reduction for deploying a new liquidity pool.

Introduction of Hooks!

Uniswap v4 introduces the concept of "hooks," which offer developers the ability to customize liquidity pools. Hooks are externally deployed contracts that execute developer-defined logic at key moments in the pool's lifecycle, such as before, after, or during a swap. Hooks are widget-like add-ons to liquidity pools that enable increased functionality and features.

These hooks allow for custom implementations such as dynamic fees, on-chain limit orders, advanced oracles, and novel liquidity strategies, traditionally predefined by the protocol like in v3. This level of flexibility enables developers to harness and innovate on Uniswap's liquidity and security, tailoring the trading experience to their specific requirements.

One notable example is the utilization of hooks to create a time-weighted average market maker (TWAMM), which addresses the challenge of minimizing price impact when executing large orders in automated market makers (AMMs). By breaking up large orders over time, TWAMM, implemented as a hook, offers a sophisticated solution to enhance trading strategies.

Fragmented Liquidity

Expanding on the "opinions" that the core Uniswap team made on Uniswap V3, protocols that wanted to modify the core parameters previously had to fork the Uniswap codebase. This often led to fragmented liquidity and increased transaction costs due to the augmented on-chain computations required, as each asset pair operated as its own contract.

Now, protocols can leverage hooks, simplifying the implementation process to fit their specific criteria without needing to fork the codebase. Ultimately, hooks significantly enhance liquidity management and trading for traders and providers.

Hooks extended use Cases:

In addition to TWAMM, hooks unlock a multitude of possibilities for customization, such as:

Dynamic Fee Structures: Hooks enable the implementation of dynamic fees that can be based on various factors, such as market volatility or other user-defined inputs. This flexibility allows for fee adjustments that align with changing market conditions.

Onchain Limit Orders: With hooks, users can leverage on-chain limit orders, enhancing the trading experience by enabling precise execution at predetermined price levels. This feature brings greater control and efficiency to trading on Uniswap.

Enhanced Liquidity Deployment: Hooks offer the ability to deposit liquidity outside the typical price range of a pool into lending protocols. This feature expands liquidity providers' options, allowing them to optimize their capital allocation and explore additional yield-generating opportunities.

Customized Onchain Oracles: Through hooks, developers can integrate customized on-chain oracles. These oracles provide alterNative price feeds and data aggregation methods, enabling the creation of innovative trading strategies and improved accuracy in determining asset prices.

Auto-compounding LP Fees: Hooks make it possible to automatically compound LP (liquidity provider) fees back into the LP positions. This feature streamlines the process of compounding earnings, optimizing returns for liquidity providers without requiring manual intervention.

Internalized MEV Profit Distribution: Hooks facilitate the internalization of Miner Extractable Value (MEV) profits, ensuring that these profits are distributed back to liquidity providers. This mechanism enhances liquidity provision incentives and aligns market participants' interests.

Reintroduction of Native ETH Support

Uniswap v4 brings back support for Native ETH, which was previously removed in v2 due to implementation complexity and liquidity fragmentation. The introduction of flash accounting and the singleton contract enables the efficient handling of Native ETH by transferring assets only on net balances. This results in significant gas savings, as Native ETH transfers are approximately half the cost of ERC-20 transfers. Although the handling of Native ETH remains a challenging area, the benefits it brings in terms of reduced gas costs make it a valuable addition to Uniswap v4.

Summary and Conclusion

Here is a wrap up of what Uniswap V4 is all about:

Uniswap v4 introduces hooks, enabling customization of liquidity pools and trading experiences.

Hooks allow the execution of custom code at specific points during a pool's execution.

Customizability empowers builders to create unique trading experiences and break free from predefined rules.

Uniswap v4 features improved gas efficiency with a singleton implementation and flash accounting.

Native ETH support is reintroduced, bringing significant gas savings.

Hooks enable a variety of use cases, including TWAMM, dynamic fee structures, on-chain limit orders, enhanced liquidity deployment, customized on-chain oracles, auto-compounding of LP fees, and internalized distribution of MEV profits.

Uniswap v4 improves DEX landscape by offering greater customization and flexibility.

These new features and improvements have the potential to enhance the efficiency of Uniswap. But the added complexity may require a steep learning curve and potentially limit adoption among less tech-savvy users. It's also important to note that Uniswap v4 will not replace v2 and v3. Each version has its unique features and improves on the earlier versions. The decision to use v2, v3, or v4 will depend on a user's specific needs and understanding. Uniswap v4 represents a step forward in terms of possibilities, and it also shows the inherent trade-off between efficiency and user-friendliness in the DeFi space. It will depend on front-end implementations to see how end users can interact without deeper understanding.

Sources

https://github.com/Uniswap/v4-core/blob/main/whitepaper-v4-draft.pdf

Not financial or tax advice. The purpose of this newsletter is purely educational and should not be considered as investment advice, a request to buy or sell any assets, or a suggestion to make any financial decisions. It is not a substitute for tax advice. Please consult with your accountant and conduct your own research.

Disclosure. All of my posts are my own, not the views of my employer.

| A guest post by

|